Strong weekly close near highs for markets after a long time

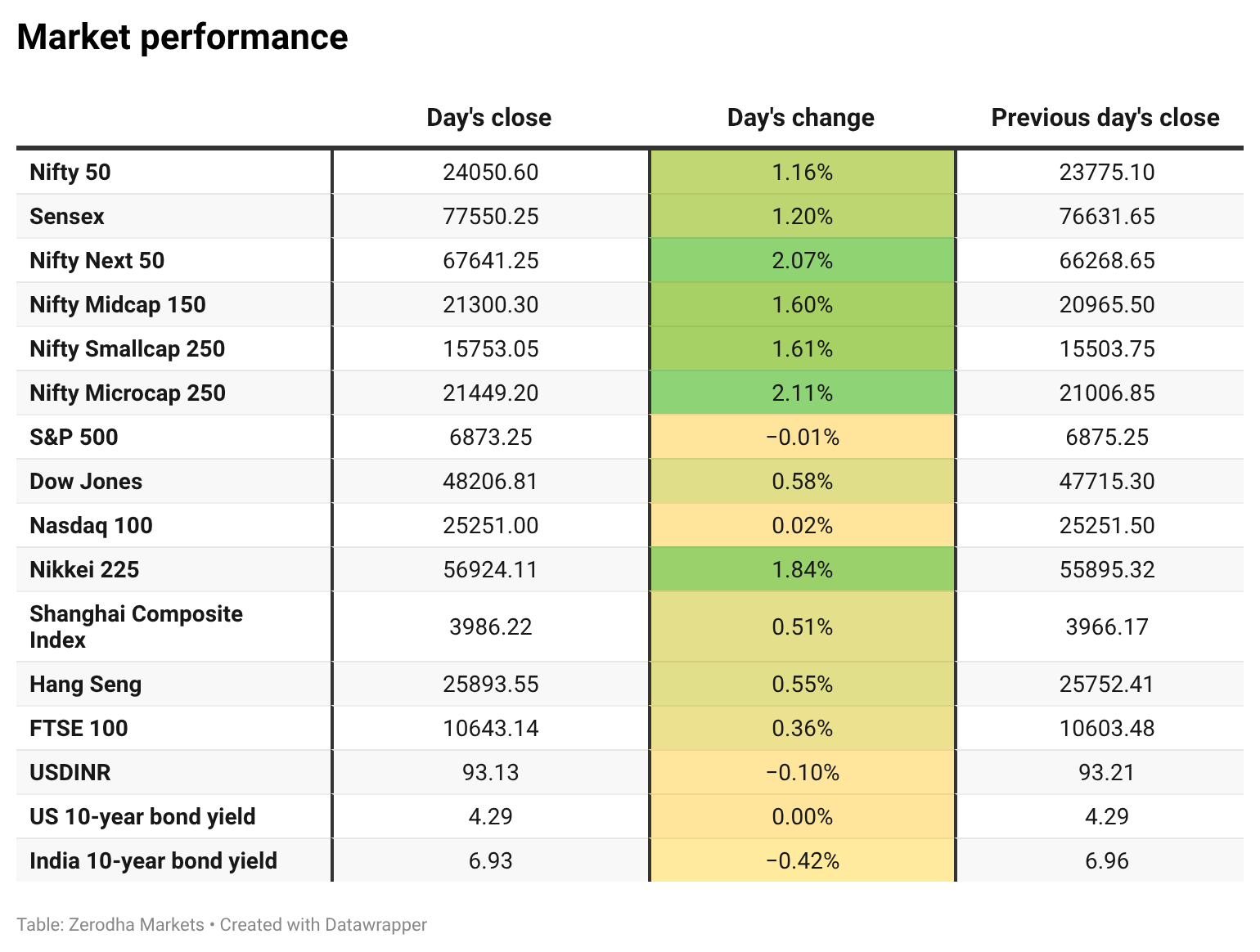

Nifty closes at 24,050 ; Broader markets continue to accelerate

Welcome to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets, both in India and globally.

In our latest episode of In The Money by Zerodha video series, we move from the "what" to the "how." Once you understand market structure, the most critical decision is execution—how to select the right strikes and define entries and exits that are repeatable. We explore why trading 1-strike In-The-Money (ITM) options based on Synthetic Futures is often the most robust rule of thumb for both buyers and sellers.

We also break down the three distinct time segments of the trading day—S1, S2, and S3—and the specific setups that emerge in each. Whether it’s a morning breakout or an afternoon mean reversion, the goal is to align your setup with the current market regime. As we discuss in the video, the primary signal must always come from the Spot chart, even when you are trading options.

Market Overview

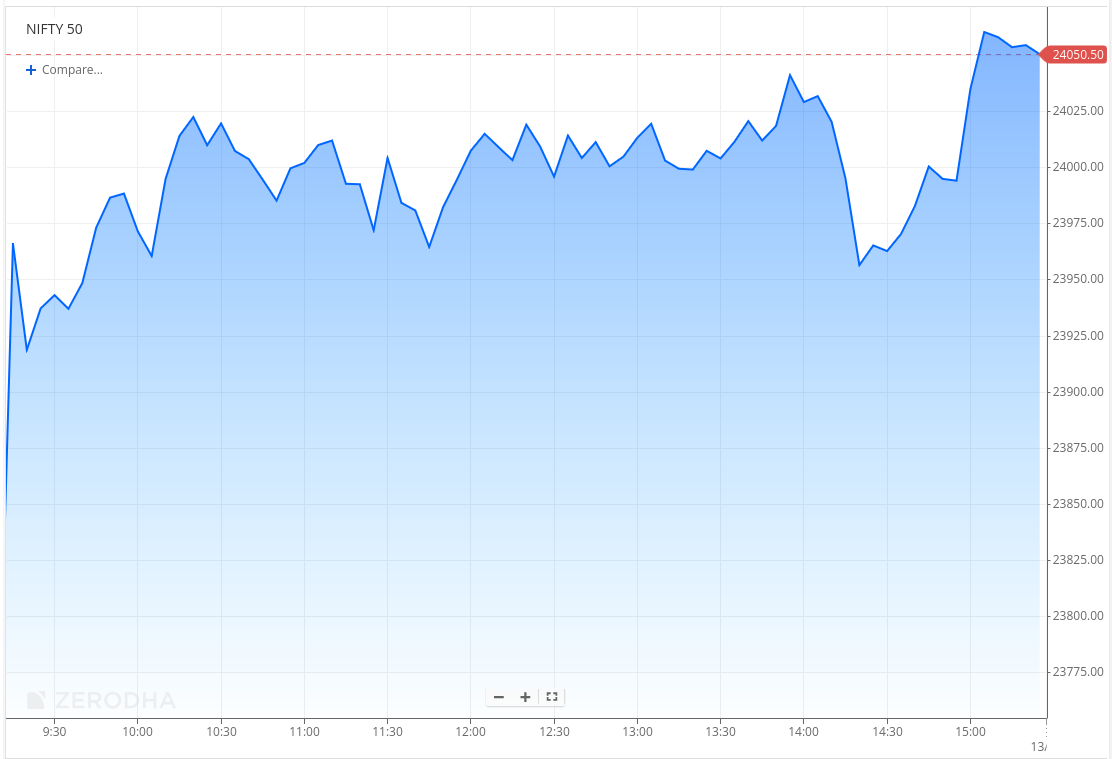

Nifty opened with a gap up of 110 points at 23,880, tracking stable global cues. The index saw some initial volatility in the opening minutes, briefly dipping toward the 23,850 zone before recovering and moving higher toward 24,000 within the first hour.

Through the late morning session, Nifty remained range-bound, oscillating between 23,950 and 24,050, with no clear directional bias. The index attempted to build on gains but faced intermittent profit booking near the 24,025 zone.

In the second half, the index continued to trade sideways, holding within a tight band as both buyers and sellers lacked conviction. A brief bout of weakness around 2 PM dragged Nifty toward the 23,950 zone, but it quickly recovered.

In the final hour, buying interest picked up, pushing the index toward the day’s highs near the 24,050–24,070 zone. Nifty eventually closed at 24,050.60, marking a strong opening and positive close to the week characterised by range-bound action for most of the day, followed by a late push higher.

Looking ahead, markets are likely to remain sensitive to global geopolitical developments, risk appetite, and key domestic cues.

Broader Market Performance:

The broader market had a super strong bullish session today. Of the 3,342 stocks that traded on the NSE, 2,667 advanced, 575 declined, and 100 remained unchanged.

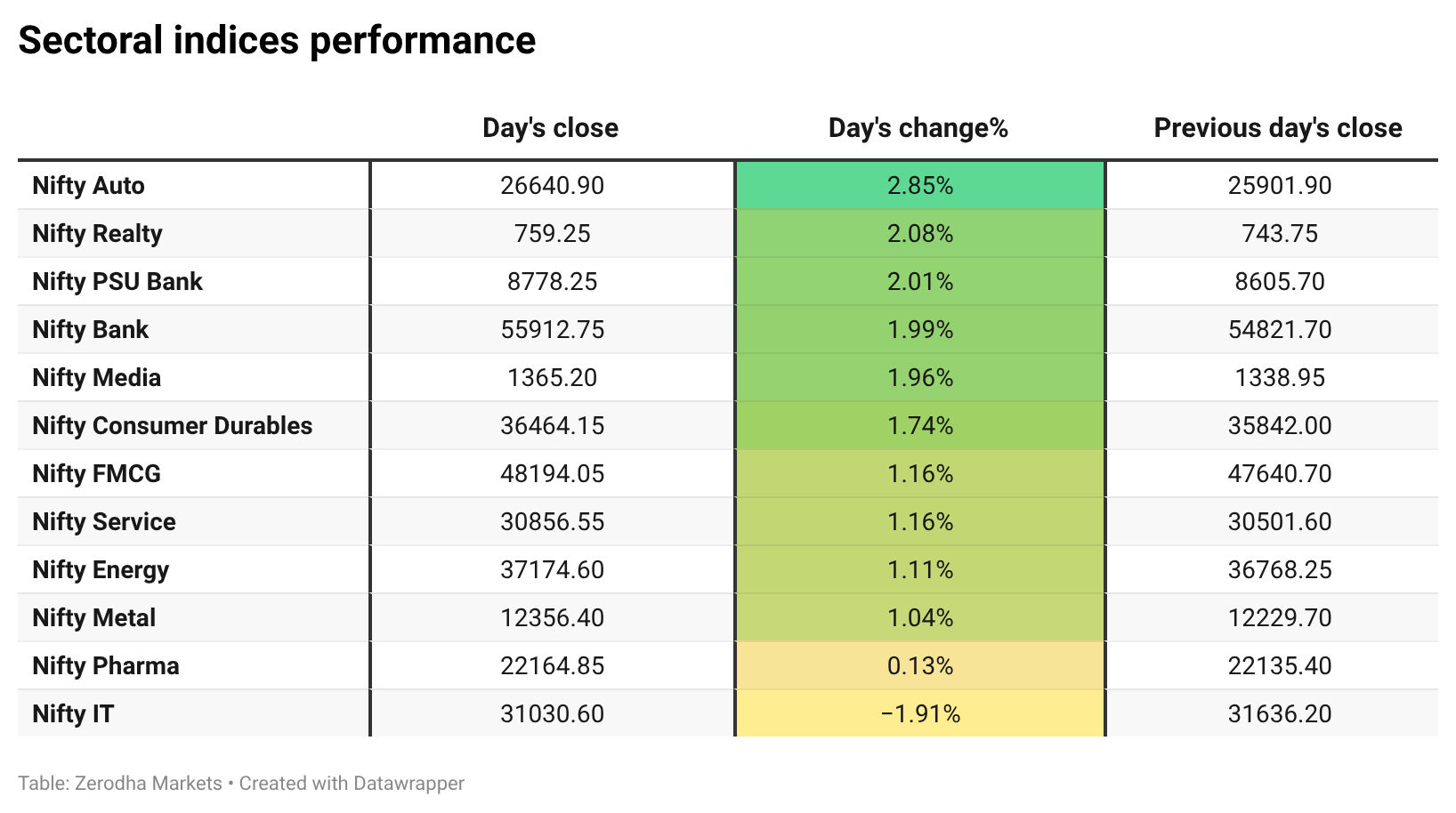

Sectoral Performance:

Nifty Auto was the top gainer, rising 2.85%, while Nifty IT was the top loser, down 1.91%. Overall, 11 sectors closed in green and 1 sector ended in red.

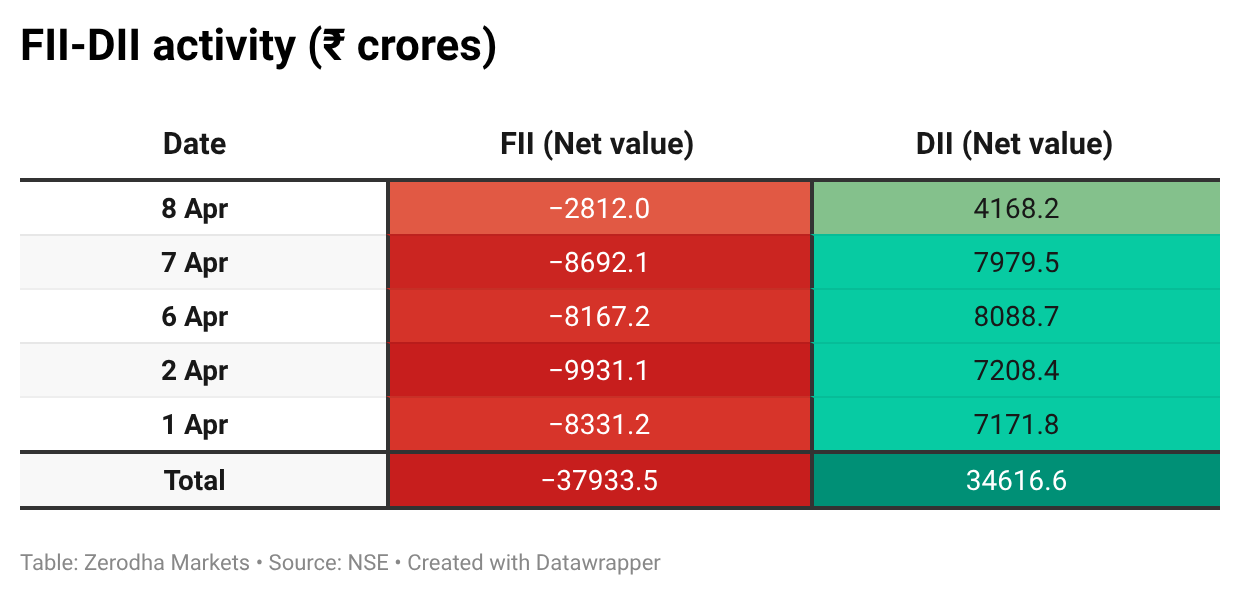

Here’s the trend of FII-DII activity from the last 5 days:

Change in OI for the day

The following is the change in OI for Nifty contracts expiring on 13th April:

The maximum Call Open Interest (OI) is observed at 24,500, followed by 24,000 & 24,300, indicating potential resistance at the 24,200 -24,300 levels.

The maximum Put Open Interest (OI) is observed at 24,000, followed by 23,900 & 23,800, suggesting support at 23,900-23,800.

Note: OI is subject to multiple interpretations; however, generally, an increase in Call OI indicates resistance in a falling market, while an increase in Put OI indicates support in a rising market.

Source: Sensibull

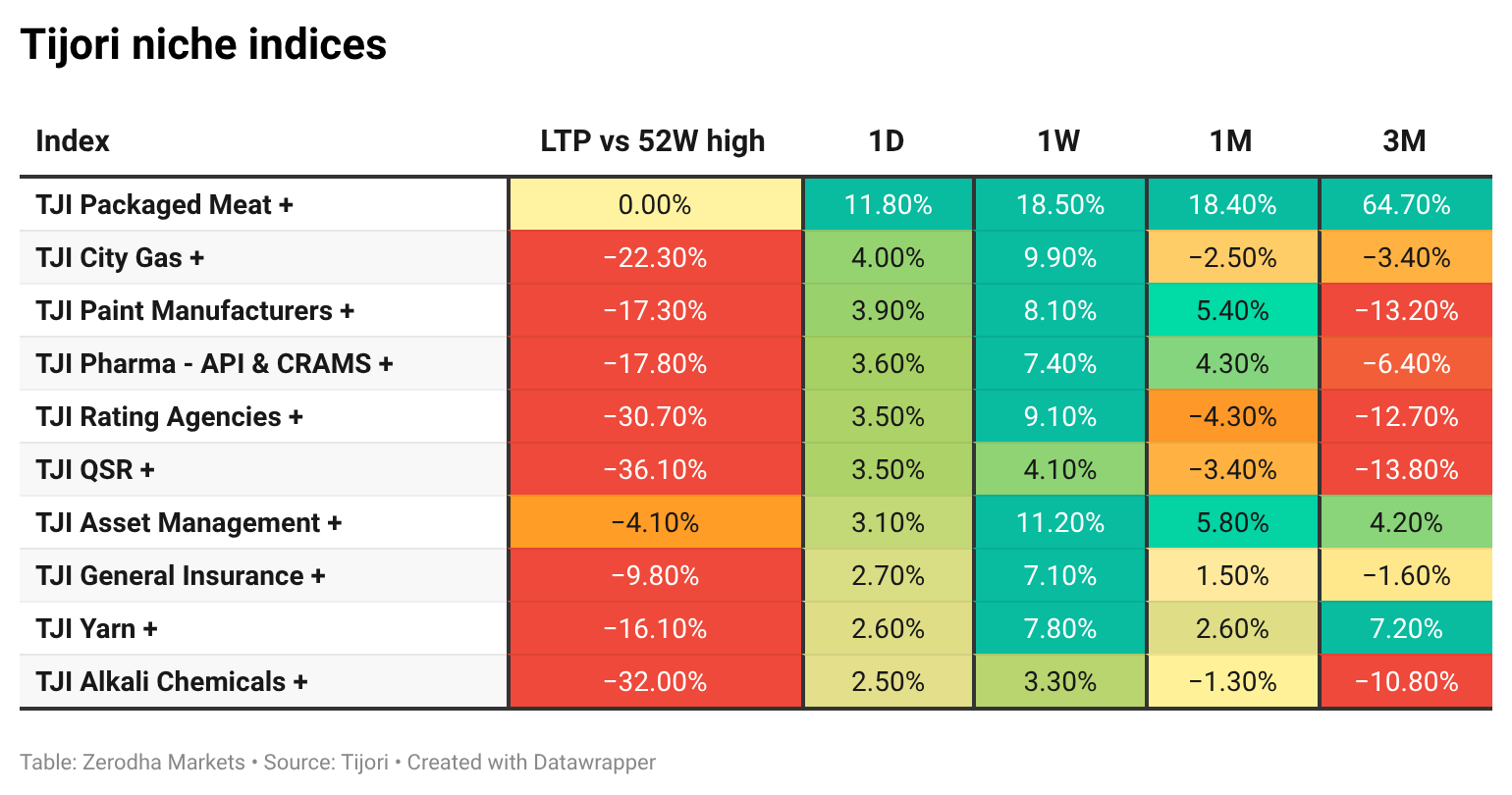

Tijori is an investment research platform that has constructed niche indices for various themes and sub-sectors. They help you understand the market performance of narrow slices of the market. You can also track the Promoter buying and other interesting stuff, like Capex activity by the companies in the Tijori App’s idea dashboard

What’s happening in India

The rupee rose 10 paise to 92.41 per dollar in early trade, supported by near-term buying. However, volatility remains high amid global tensions and the RBI’s deadline on banks’ forex positions. Dive deeper

India’s 10-year bond yield rose to around 6.97% as a rebound in crude prices renewed inflation concerns. Upcoming government bond supply and positioning ahead of auctions also added pressure on yields. Dive deeper

India’s forex reserves rose sharply by $9.06 billion to $697.12 billion for the week ended April 3, reversing the prior week’s decline. Despite the rebound, reserves remain below the record high of $728.49 billion seen in late February, before the West Asia conflict. Dive deeper

E-way bill generation hit a record 140.6 million in March 2026, up 13% YoY and 6% sequentially, signalling strong economic activity. The sustained rise follows GST rate rationalisation, with volumes consistently hitting new highs. Dive deeper

Jaypee Group founder Jaiprakash Gaur has backed Adani Group’s ₹14,535 crore takeover of Jaiprakash Associates, calling the resolution process fair and transparent. Dive deeper

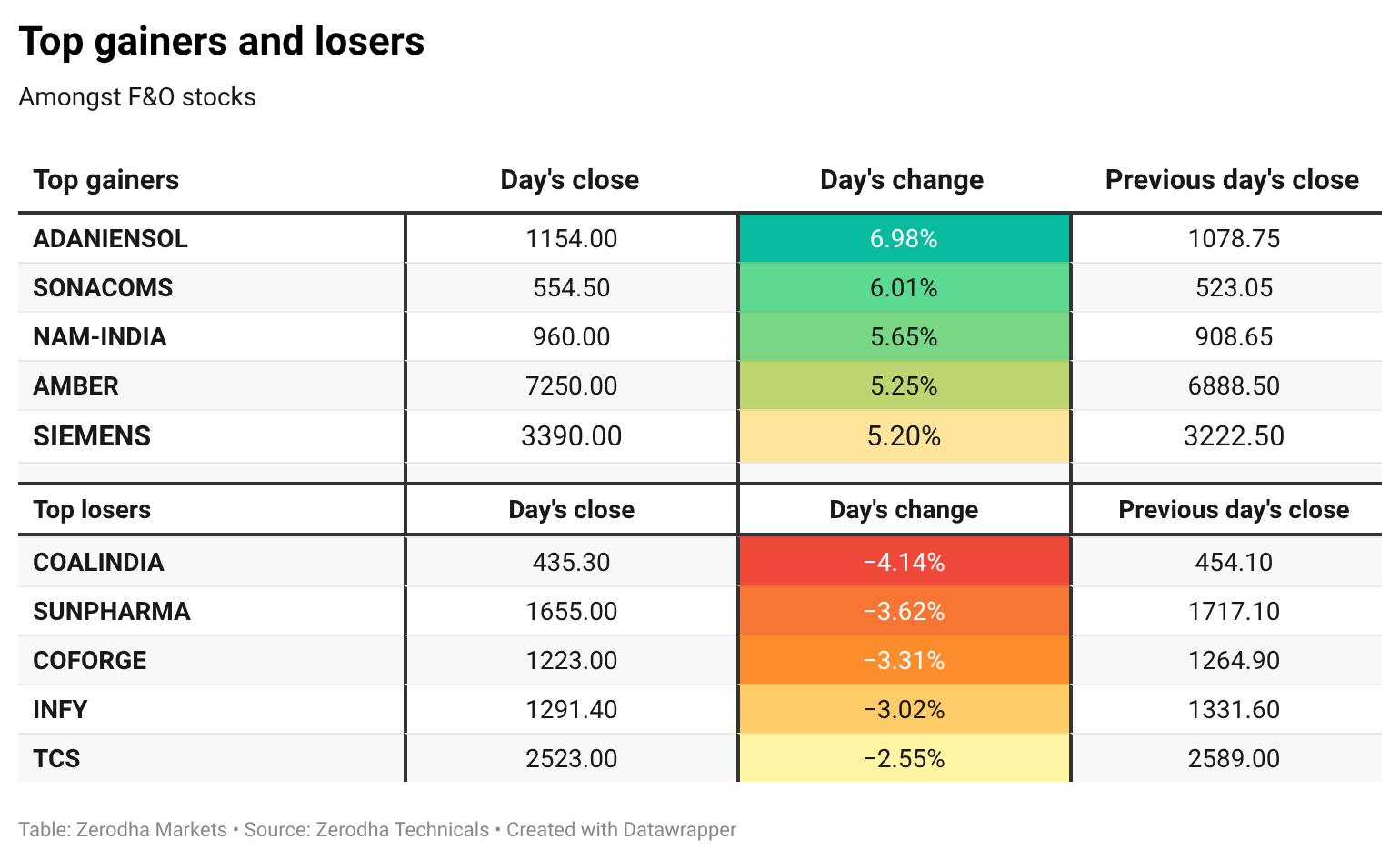

TCS shares fell nearly 3% despite a quarterly earnings beat, as a rare annual revenue decline weighed on sentiment. Dive deeper

RBI to absorb ₹2 lakh crore liquidity via VRRR auction, targeting surplus liquidity of ₹4.55 lakh crore in the banking system. The move pushed 10-year bond yield higher, signaling tighter near-term liquidity conditions. Dive deeper

RailTel shares were in focus after securing a ₹23.18 crore order to develop an online portal for the Goa Construction Workers Welfare Board. Dive deeper

Ola Electric shares surged over 12% after announcing readiness of its in-house LFP battery cell, extending gains for a third session. Dive deeper

What’s happening globally

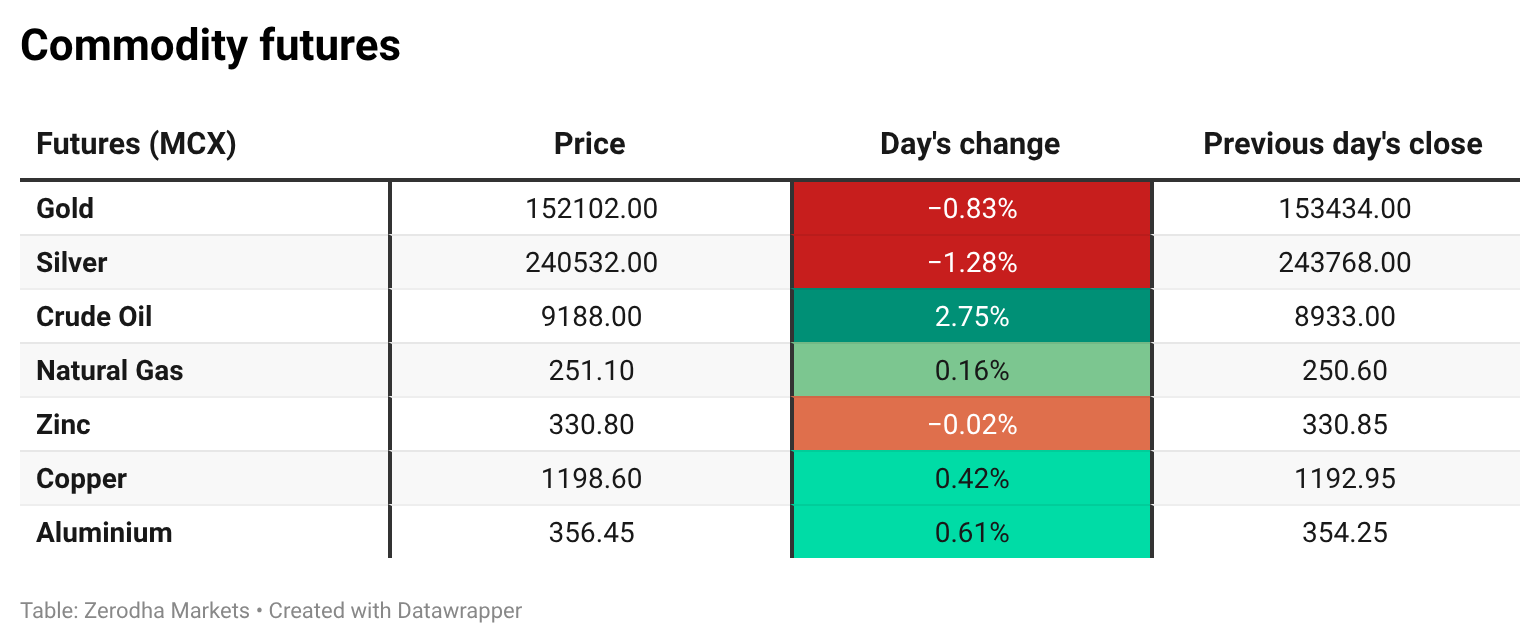

WTI crude rose above $98/bbl amid fresh Middle East tensions and Hormuz disruption fears, despite ongoing ceasefire talks. Dive deeper

Gold held above $4,700/oz, set for a third weekly gain as easing oil prices reduced inflation fears. A softer dollar and ongoing geopolitical uncertainty continued to support demand. Dive deeper

US inflation likely rose to 3.3% in March, highest since May 2024, driven by a surge in energy prices. Monthly CPI jumped 0.9%, fastest since 2022, while core inflation edged up to 2.7%. Dive deeper

Euro rose above $1.17, nearing a 1.5% weekly gain, supported by Russia-Ukraine peace optimism. Dive deeper

Japan’s 10Y bond yield rose to 2.4%, near its highest since 1998, on rising BOJ rate hike expectations. Dive deeper

China’s producer prices rose 0.5% YoY in March, ending a long deflation streak and beating expectations. Dive deeper

Management chatter

In this section, we highlight interesting comments from the management of major companies and policymakers in the Indian and Global Economies.

Arun Kumar Singh, Chairman and CEO of ONGC on the current crisis:

“Thinking that West Asia is nearest to us and therefore all their resources (can be accessed easily), we should take it with a pinch of salt,”

“A paradigm shift has happened, If the world gets more and more de-globalised, we will have more and more problems.”

“For the next 30-40 years… if you have multiple (powers), then you have an everyday… war of supremacy.” - Link

Andy Jassy, Chief Executive Officer, Amazon on AI:

“Annualised revenue from AI services at AWS exceeded $15 billion.”

“The AI revenue run rate is ascending rapidly.”

“We’re not investing approximately $200 billion in capex on a hunch.” - Link

🧑🏻💻Have you checked out The Chatter?

Every week, we listen to the big Indian earnings calls—Reliance, HDFC Bank, and even smaller logistics firms—and copy the full transcripts. We then remove the fluff and keep only the sentences that could move a share price: a surprise price hike, a cut-back on factory spending, a warning about weak monsoon sales, or a hint from management on RBI liquidity. We add a quick, one-line explainer and a timestamp so you can trace the quote back to the call. The whole thing lands in your inbox as one sharp page of facts you can read in three minutes—no 40-page decks, no jargon, just the hard stuff that matters for your trades and your macro view.

Go check out The Chatter here.

We’re now on WhatsApp!

We’ve started a WhatsApp channel for The Daily Brief where we’ll share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops, so you can read or watch it right away. Here’s the link.

See you there!

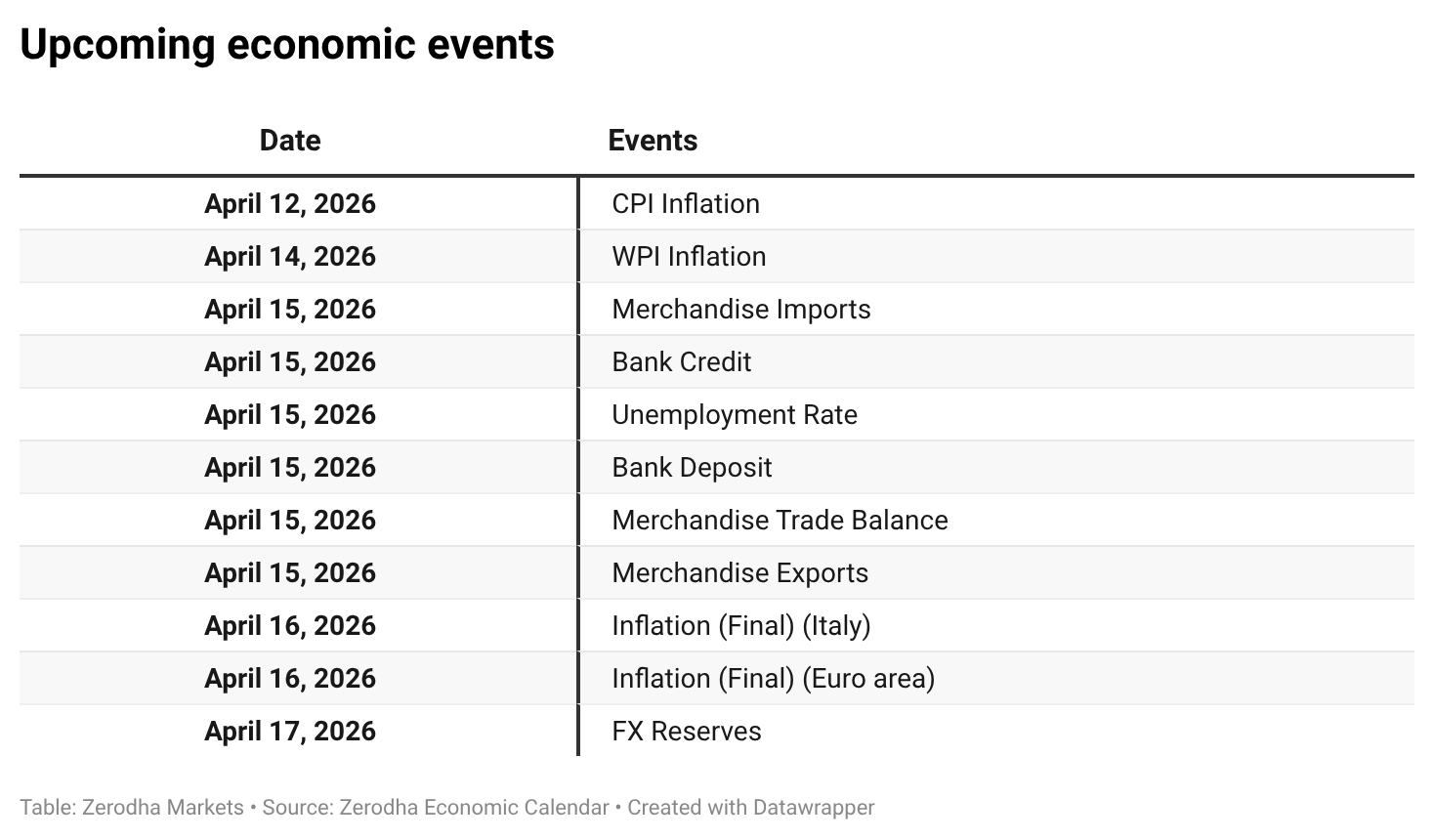

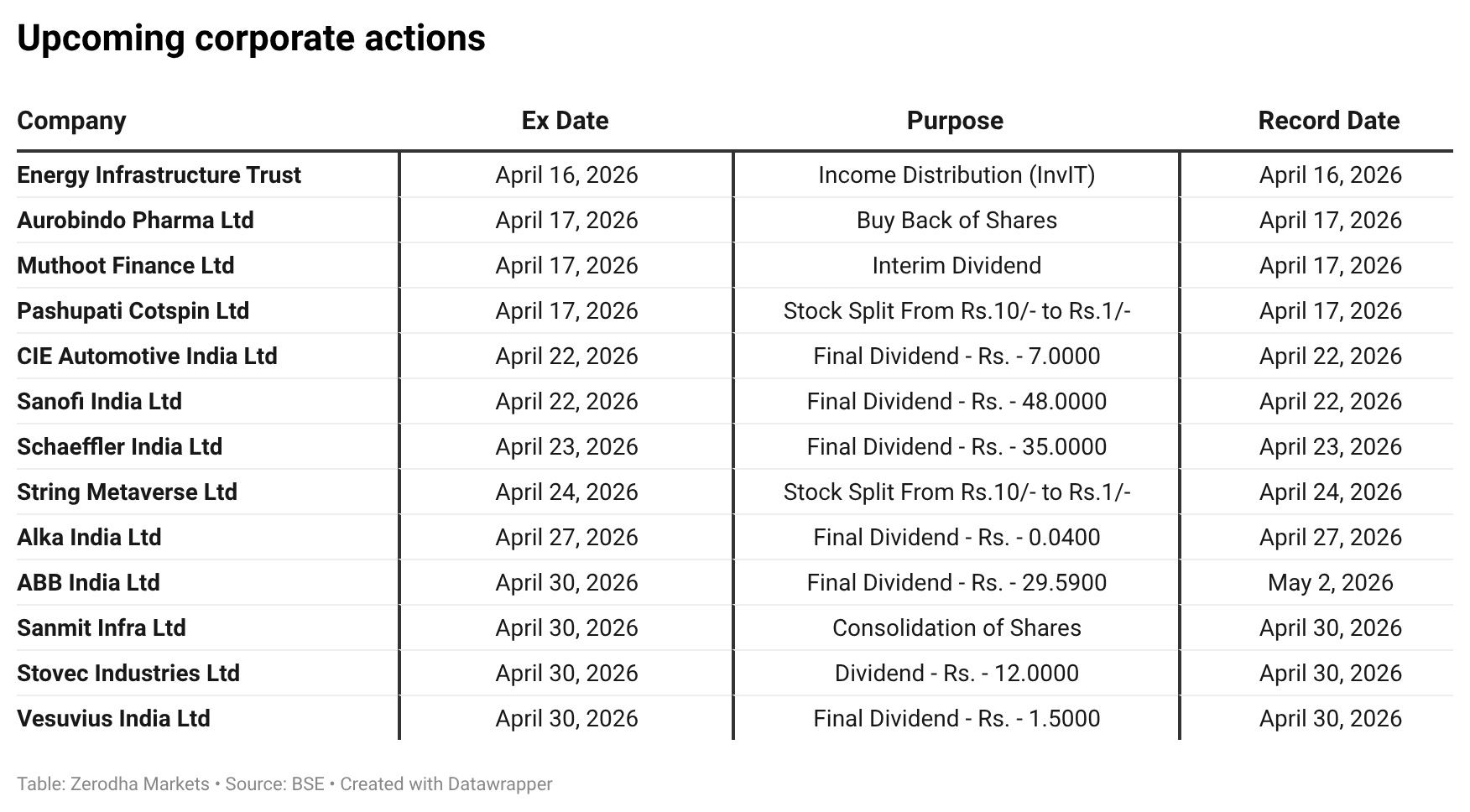

Calendars

In the coming days, we have the following significant events and corporate actions:

That’s it from us for today. We’d love to hear your feedback in the comments, and feel free to share this with your friends to spread the word!

Well shared