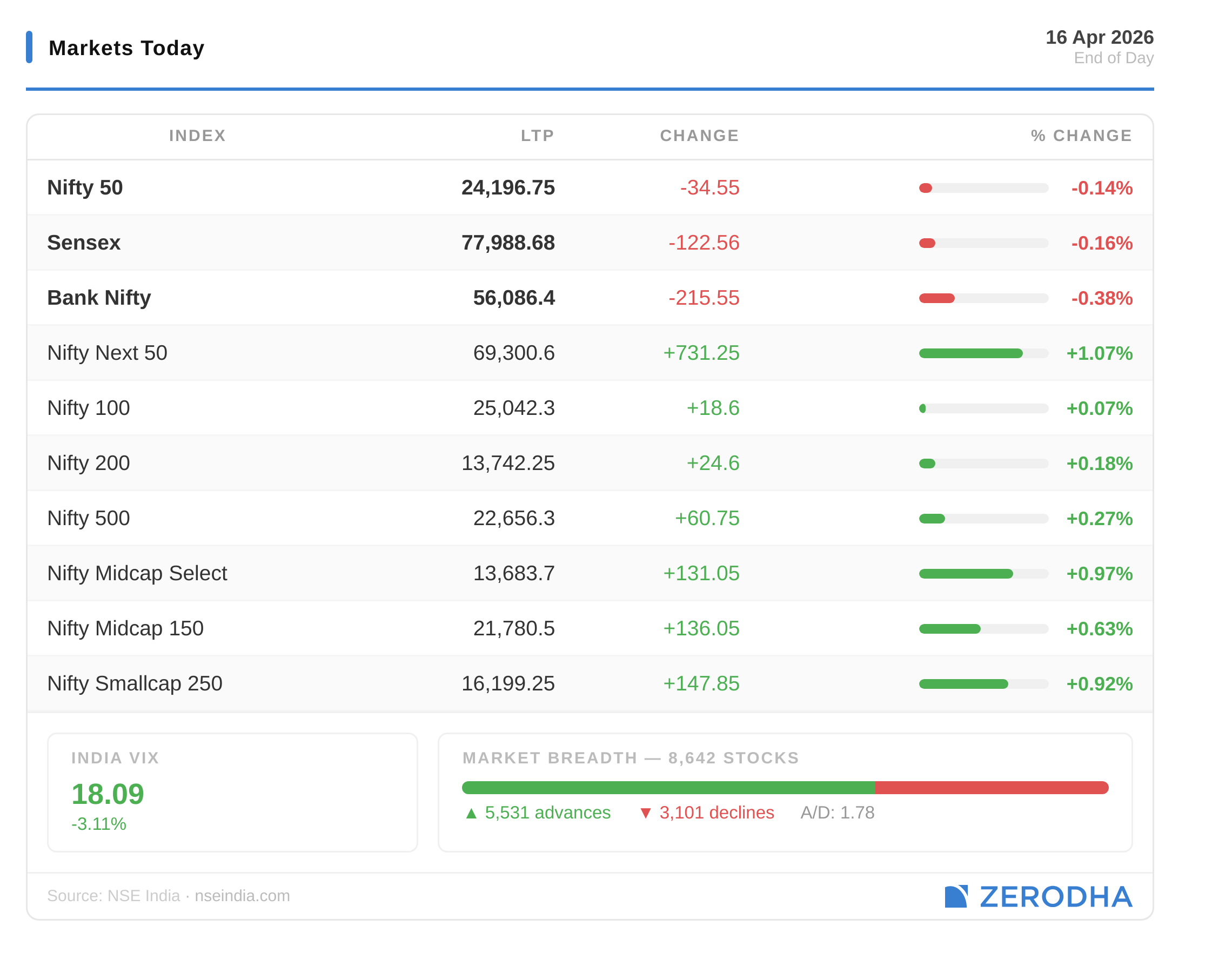

Nifty closes below 24,200 as weakness in banking stocks weigh

Broader market breadth continues to impress

Welcome to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets, both in India and globally.

In our latest episode of In The Money by Zerodha video series, we move from the “what” to the “how.” Once you understand market structure, the most critical decision is execution—how to select the right strikes and define entries and exits that are repeatable. We explore why trading 1-strike In-The-Money (ITM) options based on Synthetic Futures is often the most robust rule of thumb for both buyers and sellers.

We also break down the three distinct time segments of the trading day—S1, S2, and S3—and the specific setups that emerge in each. Whether it’s a morning breakout or an afternoon mean reversion, the goal is to align your setup with the current market regime. As we discuss in the video, the primary signal must always come from the Spot chart, even when you are trading options.

Markets Today

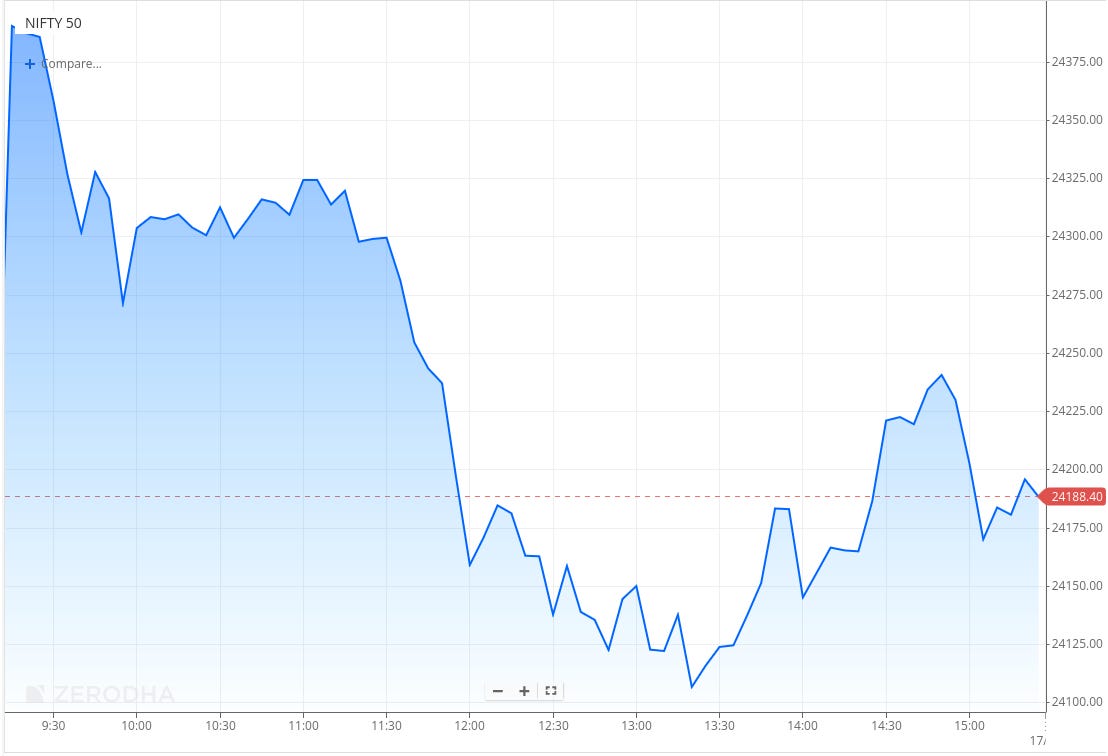

Nifty opened with a 154-point gap-up at 24,385, tracking positive global cues as the S&P 500 hit fresh record highs. However, the index came under immediate selling pressure, slipping toward the 24,270–24,300 zone within the first hour.

After trading largely range-bound until 11:30 AM, Nifty gradually drifted lower and broke below the 24,200 mark. Selling intensified around noon, dragging the index sharply to the day’s low near the 24,100 zone by 1:30 PM.

A recovery attempt followed, with Nifty rebounding toward the 24,200–24,230 range in the final hour. However, the bounce lost momentum, and the index turned choppy into the close.

Nifty eventually closed down 0.14% at 24,196.75, losing 34.55 points. Bank Nifty declined 0.38%, marking its second straight session of losses. India VIX eased 3.11% to 18.09, while market breadth turned sharply positive, with 5,531 advances versus 3,101 declines—a notable reversal from yesterday’s near-even split. Despite broad-based participation, the index remained under pressure due to weakness in banking stocks and continued to trade below its 50-day EMA of 24,282.

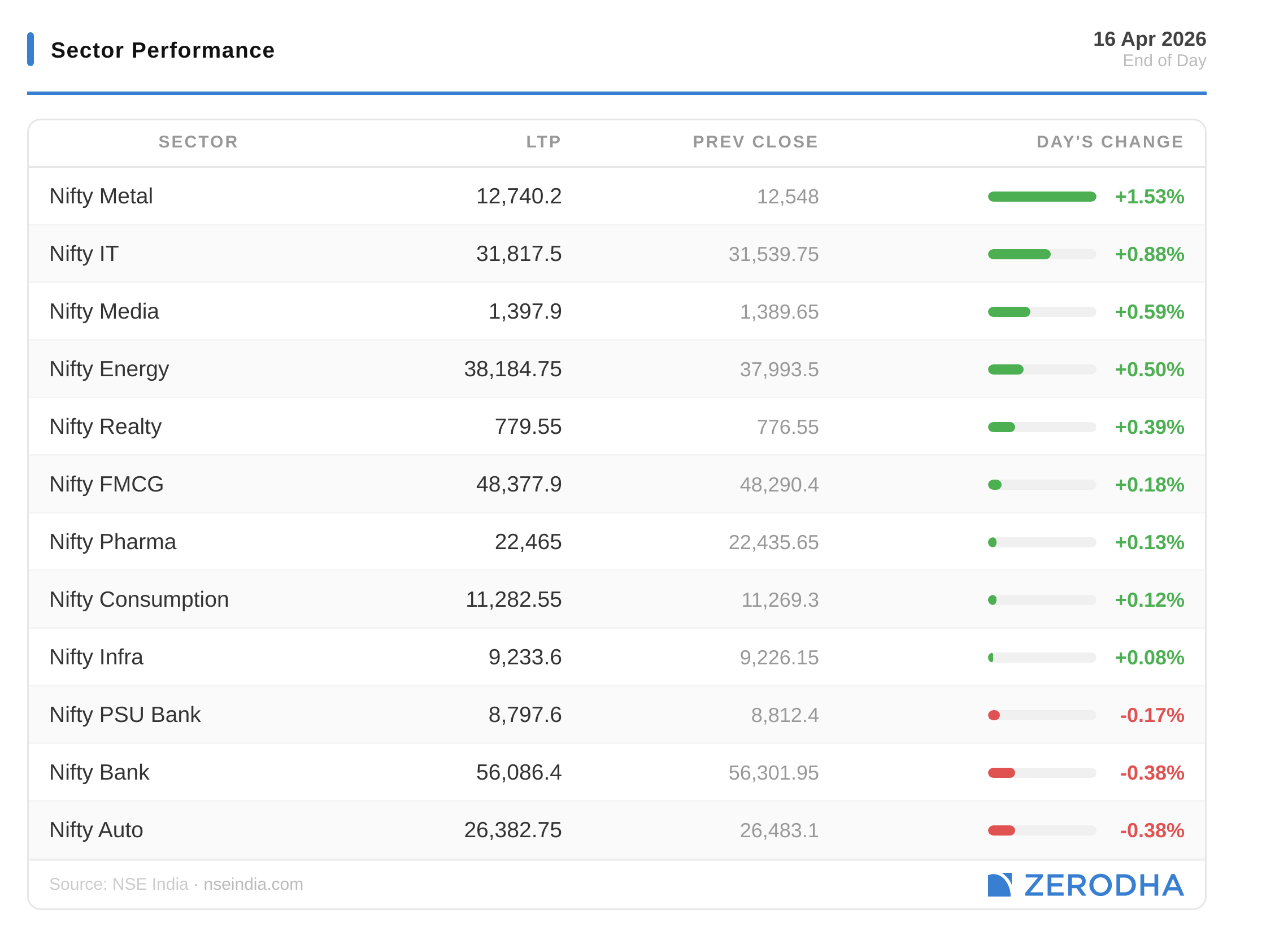

Sector Performance

Metals led for a third day, up 1.53%, extending the rally that began when FIIs returned. IT added 0.88%, Media rose 0.59%, and Energy continued its resilience at +0.5%. Bank Nifty’s 0.38% decline weighed on the headline, with PSU Bank down 0.17% and Auto down by 0.38%. Nine of 12 sectors closed green, the broadest strength since Tuesday’s full sweep.

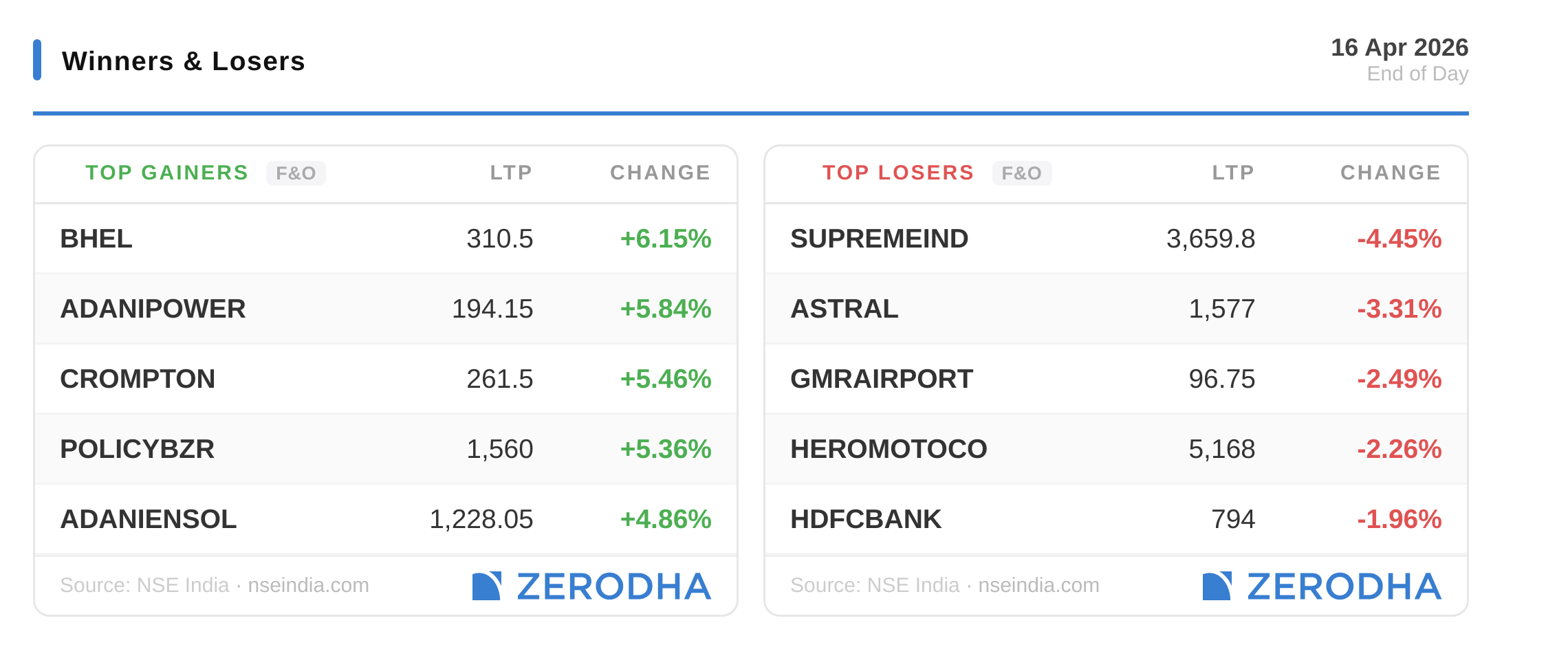

Winners & Losers

Midcap outperformed, up 0.97%, building on yesterday’s momentum as participation deepened across the market. The 5,531 advances marked the healthiest breadth of the week, a full turn from Monday’s 2,456 gainers. Broader stocks absorbed the banking weakness, with gains concentrated in metals and smaller-cap cyclicals as sentiment stabilized.

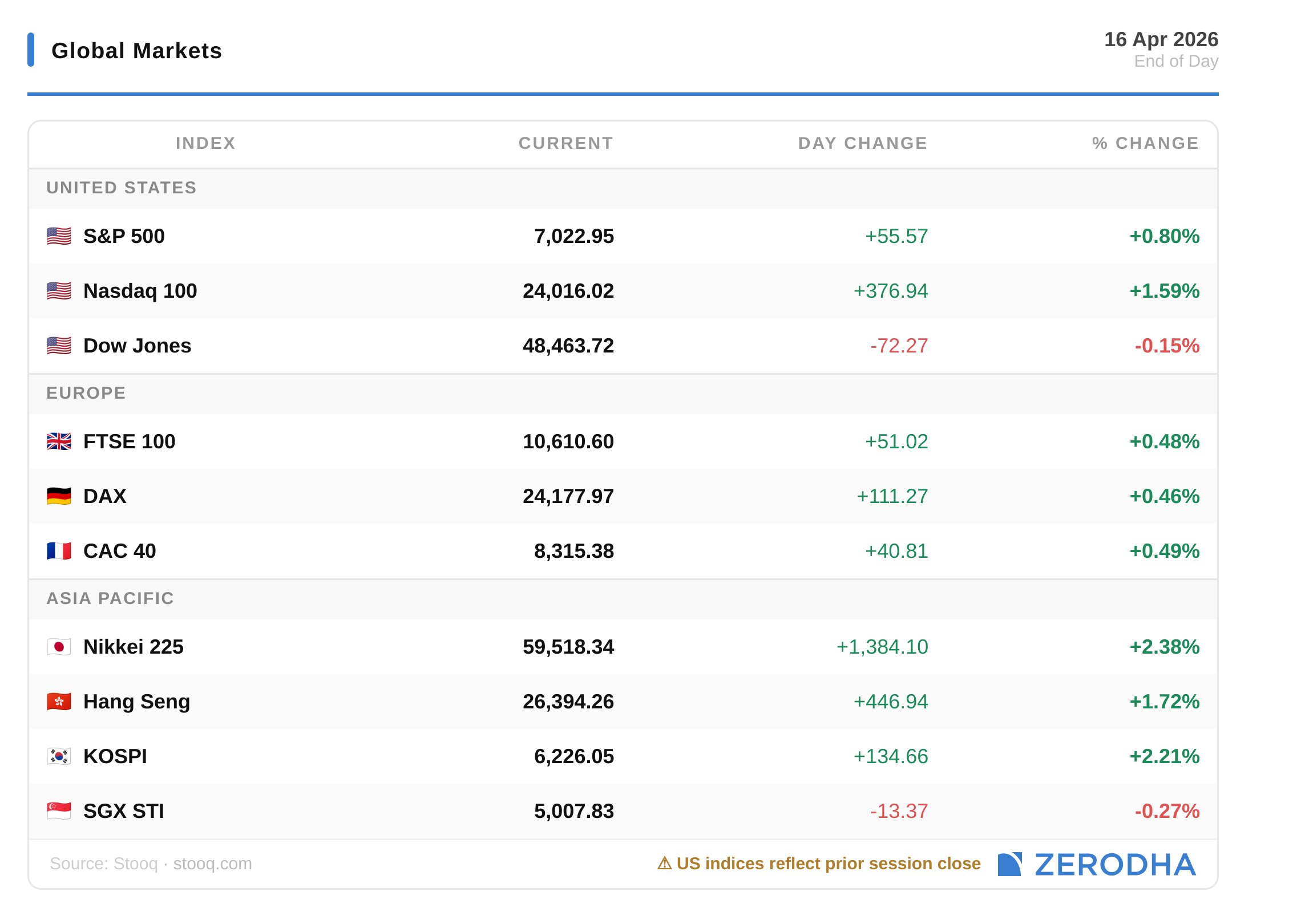

Global Markets

US markets held mixed after a strong close yesterday, ahead of key data, with the Dow underperforming slightly at 48,463 and the Nasdaq outperforming at 26,394. European indices traded with a nearly 0.5% gain. Asian markets closed with strong gains, with Hong Kong’s Hang Seng at 26,394 and Nikkei at 59,518, tracking strong global cues led by the US.

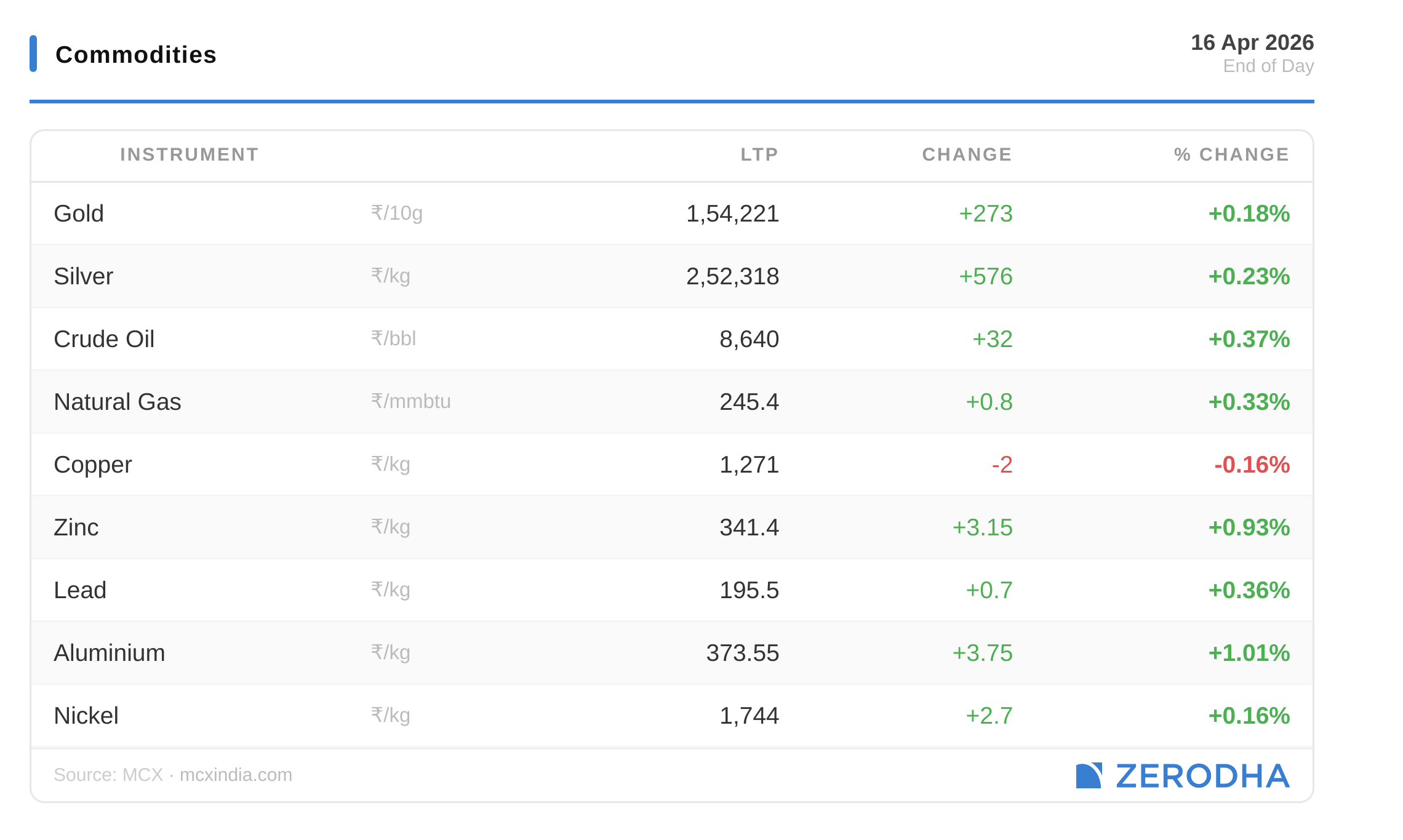

Commodities

Crude edged up 0.37% to ₹8,640 per barrel, holding steady as supply concerns persisted. Gold rose 0.18% to ₹1,54,221, and silver gained 0.23% to ₹2,52,318, both supported by softer dollar sentiment.

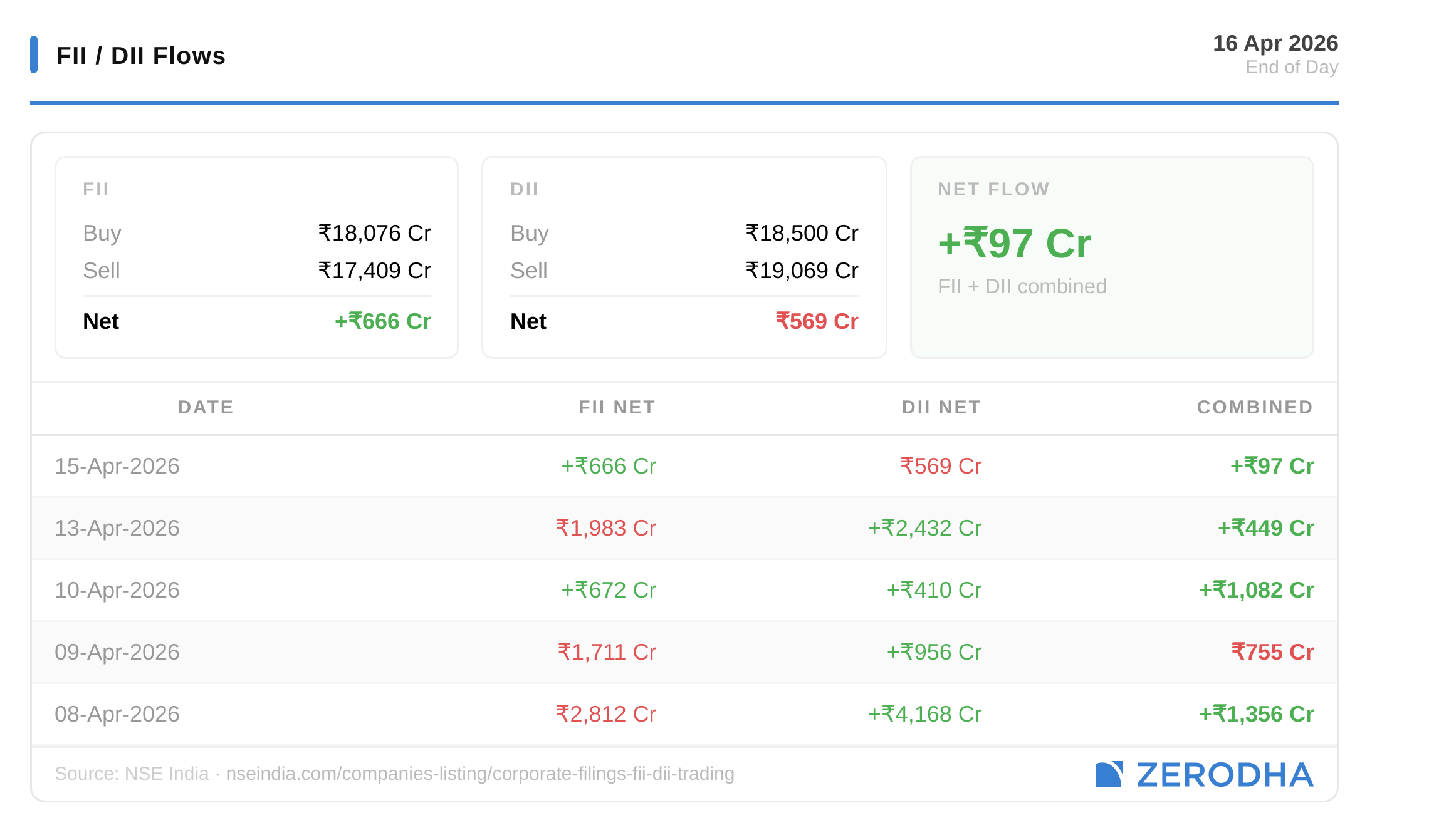

FII / DII Flows

Here’s the trend of FII-DII activity from the last 5 days:

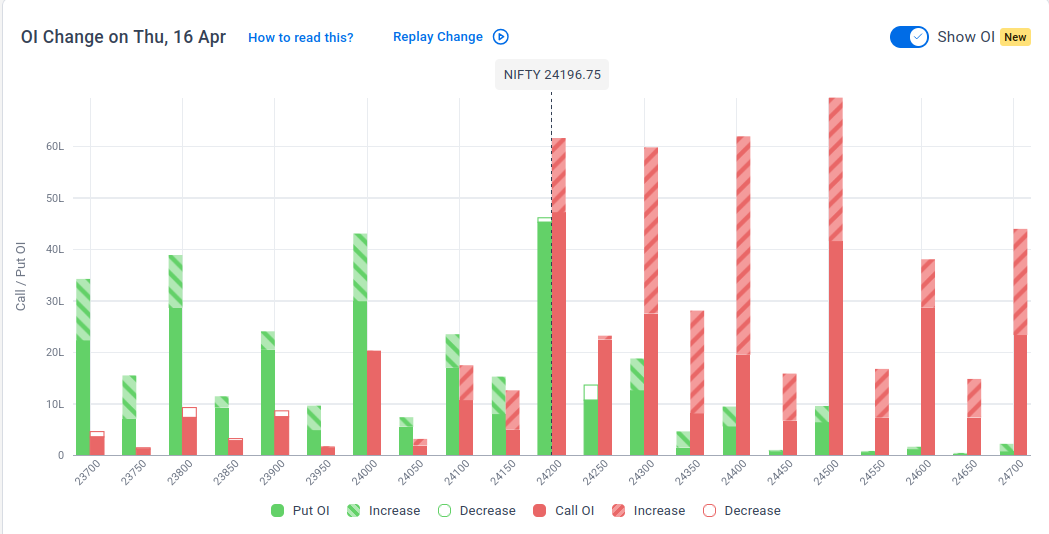

Change in OI for the day

The following is the change in OI for Nifty contracts expiring on 21st April:

The maximum Call Open Interest (OI) is observed at 24,500, followed by 24,400 & 24,200, indicating potential resistance at the 24,300 -24,400 levels.

The maximum Put Open Interest (OI) is observed at 24,200, followed by 24,000 & 23,800, suggesting support at 24,000-23,900.

Note: OI is subject to multiple interpretations; however, generally, an increase in Call OI indicates resistance in a falling market, while an increase in Put OI indicates support in a rising market.

Source: Sensibull

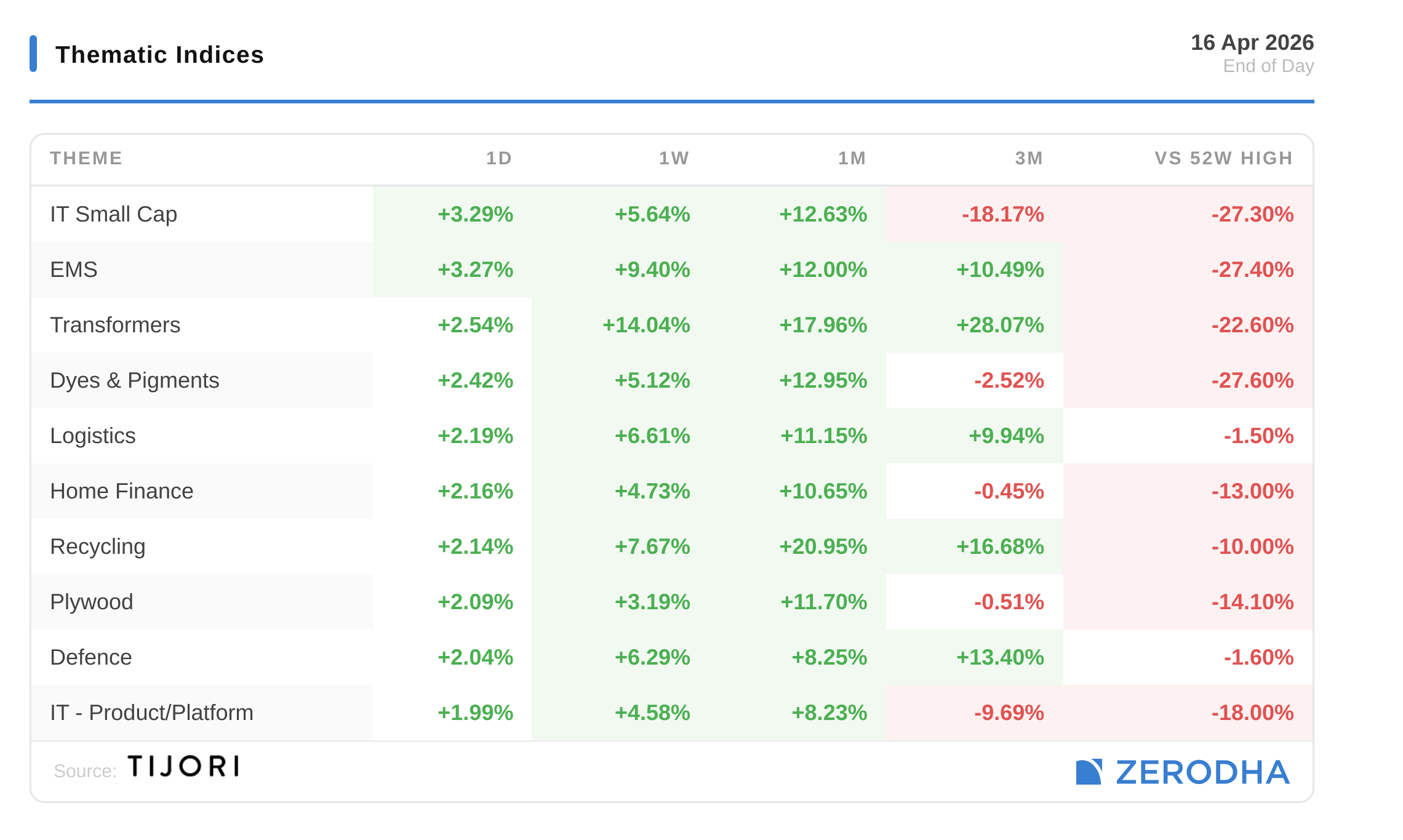

Thematic Indices

Tijori is an investment research platform that has constructed niche indices for various themes and sub-sectors. They help you understand the market performance of narrow slices of the market. You can also track the Promoter buying and other interesting stuff, like Capex activity by the companies in the Tijori App’s idea dashboard

Top Stories in India

The Indian rupee strengthened 0.2% to close at 93.20/$, supported by optimism around a potential Iran peace deal. Softer oil prices and record-high global equities also aided sentiment. Dive deeper

Wipro Limited reported a 12.3% QoQ rise in net profit to ₹3,502 crore, with revenue up 2.9% to ₹24,236 crore. However, constant currency growth remained muted at 0.2%, while margins dipped slightly to 17.3%. Dive deeper

Wipro Limited approved a ₹15,000 crore share buyback at ₹250 per share, offering a 19% premium from Current prices. Dive deeper

HDFC Life Insurance reported a 4.7% YoY rise in Q4 profit to ₹497 crore, with premium income up 9%. The company declared a ₹2.10 dividend and plans a ₹1,000 crore share issuance to HDFC Bank. Dive deeper

HDFC Asset Management Company reported Q4 net profit of ₹623 crore, down 19% QoQ but flat YoY. Revenue rose 16.5% YoY, and the board recommended a final dividend of ₹54 per share. Dive deeper

The RBI has allowed NBFCs to open branches without prior approval, unless specifically restricted. The move eases expansion norms and gives non-banking lenders greater operational flexibility. Dive deeper

An offshore oil and gas project linked to BPCL in Brazil moved closer to development after Petrobras approved the final investment decision for the SEAP-I project. The development includes an FPSO vessel with the capacity to produce 120,000 barrels of oil per day and process 10 million cubic metres of gas daily. Dive deeper

Gujarat Mineral Development Corporation shares jumped 20%, marking their sharpest single-day gain since July last year. The rally came amid strong momentum in metal stocks, with the Nifty Metal index also trading higher. Dive deeper

Brigade Enterprises Ltd said it will develop a 39-acre township project in Bengaluru with an estimated revenue potential of ₹7,200 crore. Dive deeper

Top Stories Globally

Oil is trading in a tight $93–95/bbl range as hopes of renewed peace talks cap gains, while ongoing supply risks prevent a sharp downside. Dive deeper

Aluminium futures rose above $3,650/tonne, the highest since March 2022, amid supply concerns and a projected global deficit. Disruptions at Emirates Global Aluminium’s smelter due to Iranian strikes have added to tightness. Dive deeper

The offshore yuan strengthened to 6.81/USD, a three-year high, after China reported stronger-than-expected Q1 growth of 5% YoY, boosting market sentiment. Dive deeper

European Central Bank flagged rising uncertainty from the Middle East conflict, with upside inflation risks and downside growth risks, though it remains confident in managing the situation. Dive deeper

Eurozone inflation was revised higher to 2.6% in March, the highest since July 2024, driven by a surge in energy prices, while other components like services and goods showed moderation. Dive deeper

The European Commission has proposed that Google share search data with third-party engines and AI chatbots under the Digital Markets Act. Google has opposed the move, citing privacy risks and regulatory overreach. Dive deeper

Donald Trump announced “historic” talks between Israel and Lebanon, the first in over three decades, aimed at easing tensions amid ongoing regional conflict and a fragile ceasefire. Dive deeper

The US will not renew waivers for purchases of Russian and Iranian oil, according to Treasury Secretary Scott Bessent. The move signals tighter energy sanctions even as diplomatic talks with Iran are being considered. Dive deeper

Management Chatter

In this section, we highlight interesting comments from the management of major companies and policymakers in the Indian and Global Economies.

Raamdeo Agrawal, chairman & co-founder at Motilal Oswal Financial Services, on Mark Mobius, who passed away yesterday:

Mark Mobius was a very iconic investor, especially with his Yul Brynner hairstyle. He was a brand in in his own in his own capacity. But more importantly, he was the ‘emerging market’ guru who put emerging markets on investors’ radar. Mark Mobius was way ahead of his time. He could see the rise of India, Brazil, etc., much ahead of other investors. I don't remember any other person who dedicated his life only to the emerging markets.

He was more of a mutual fund investor. That said, firstly, he believed in meeting companies personally—visiting plants, understanding operations firsthand. That’s something I also strongly believe in.

Second, he had a very independent mindset. He would invest based on his own conviction—buying during crises, investing in unpopular or ignored stocks. He wasn’t driven by market sentiment but by his own assessment of value. That independence of thought was probably his biggest strength. - Link

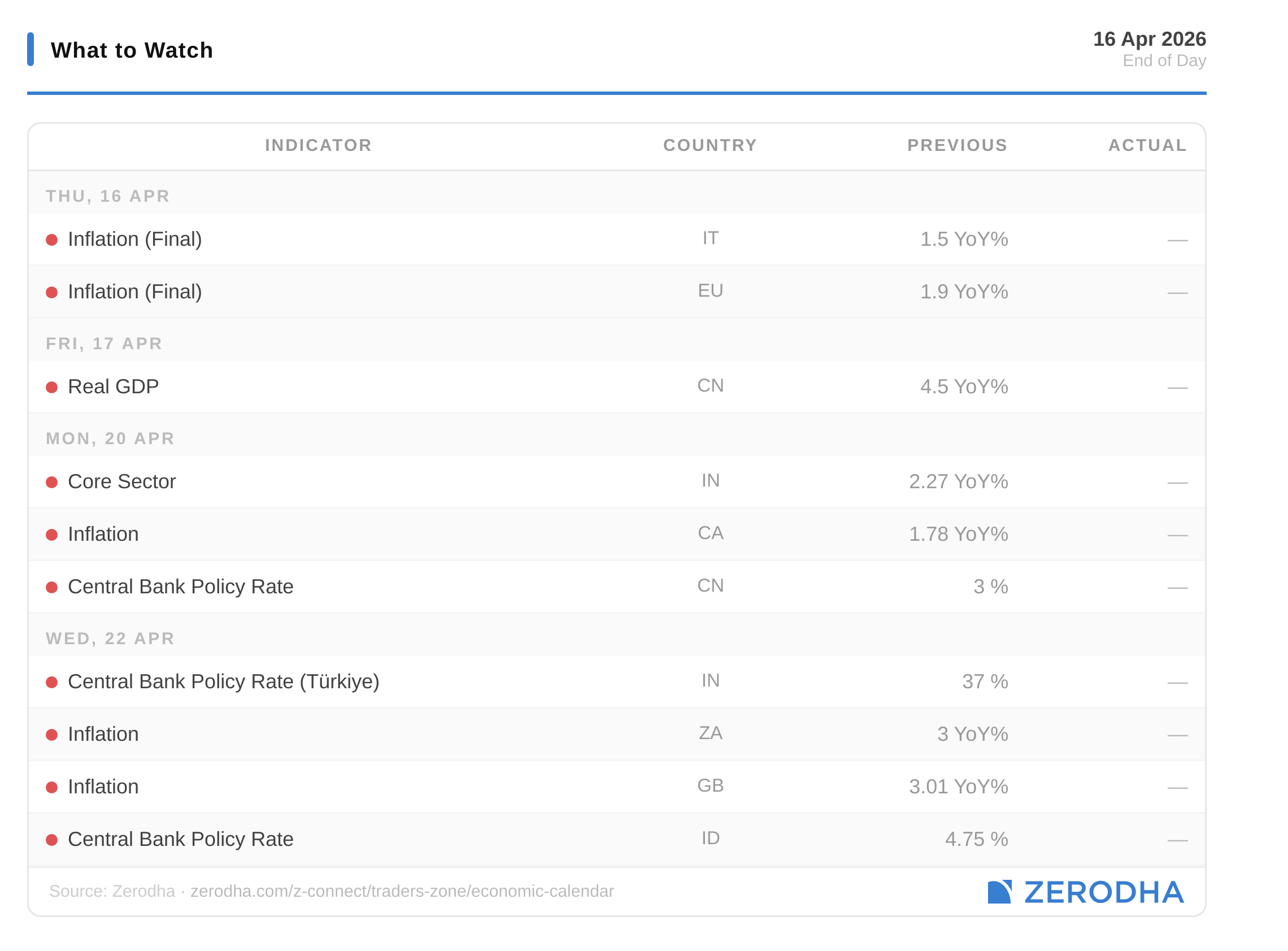

What to Watch

No major economic releases on the calendar, leaving focus on earnings and FII flow continuity as markets are likely to remain sensitive to global geopolitical developments, risk appetite, and key domestic cues.

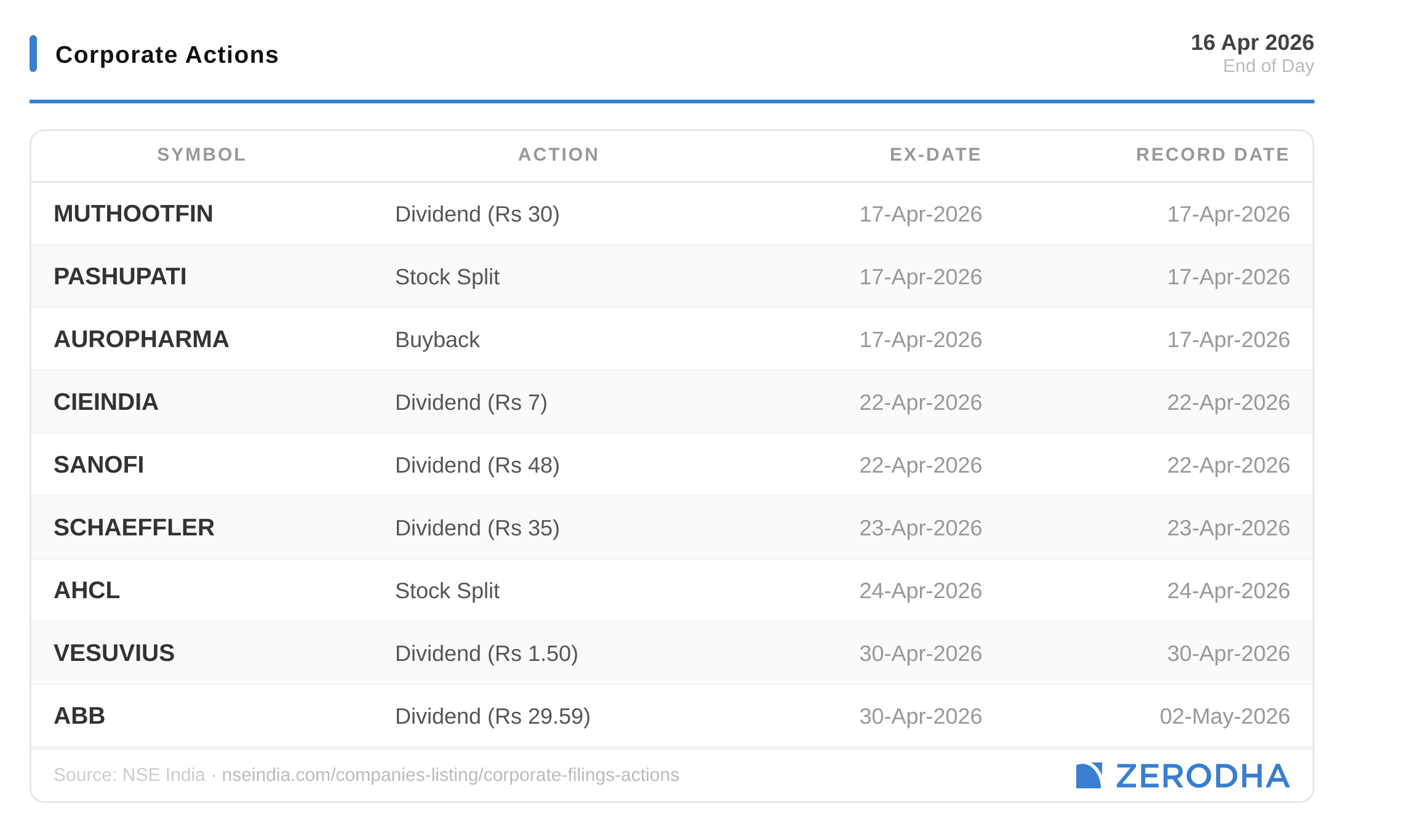

Corporate Actions

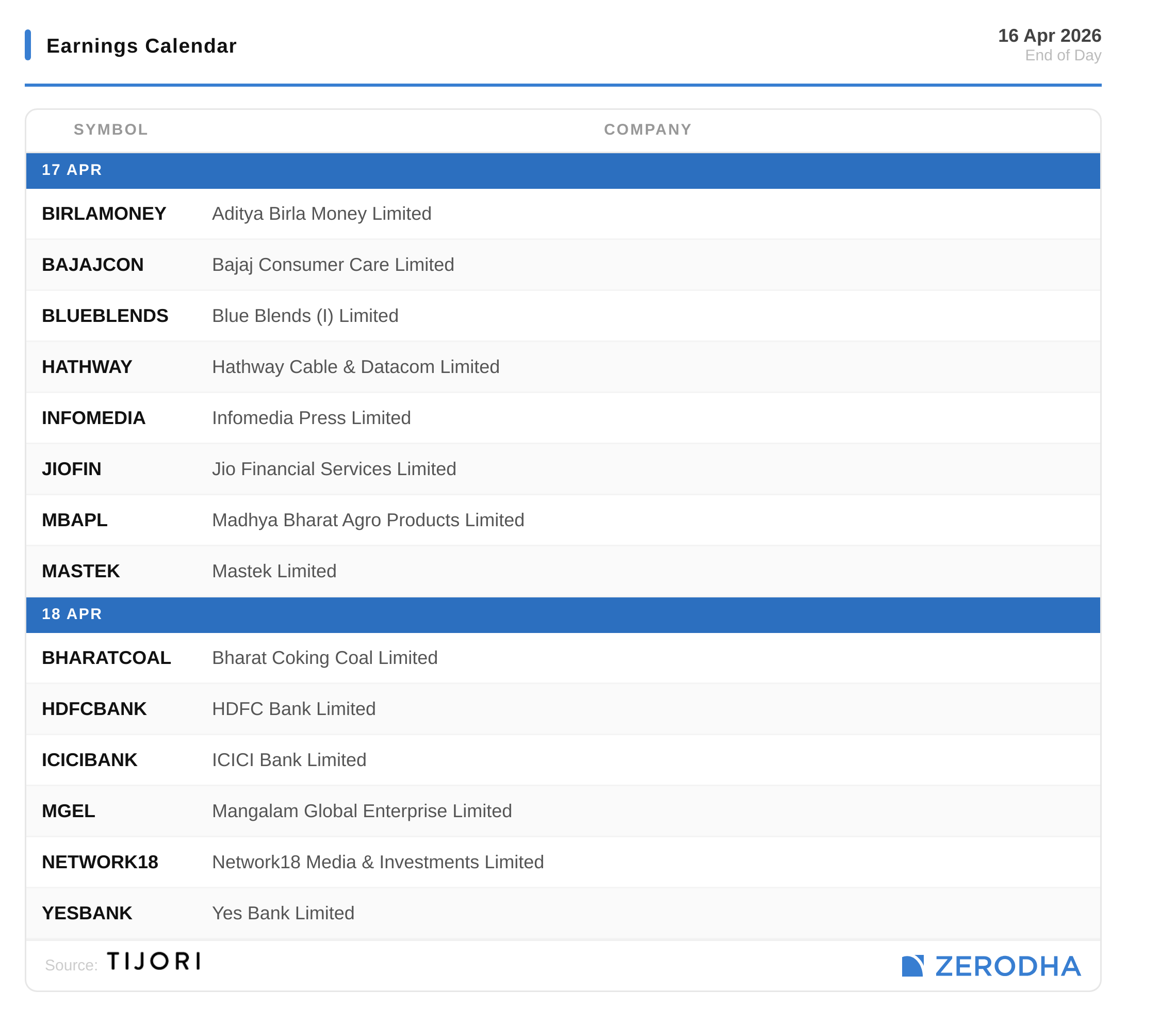

Earnings Calendar

Published by Zerodha. Not investment advice. Data from NSE, BSE, MCX.

That’s it from us for today. We’d love to hear your feedback in the comments, and feel free to share this with your friends to spread the word!

zerodha changed the images type

The new format, content and image type is excellent keep it up 👍