IT weakness and oil spike drag Nifty below 24,400

Broader markets continue to inch higher

Welcome to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets, both in India and globally.

In our latest episode of In The Money by Zerodha, from exporting and analysing trade logs from TradingView using Claude AI, to running a complete back test directly within Claude using raw OHLC data, this episode walks you through both approaches, step by step.

This episode breaks down how to move from a working strategy to a data-driven one, sweeping through multiple EMA parameters, comparing indicators like SuperTrend vs EMA, generating year and month-wise performance tables, and extracting key metrics like total points, win rate, and return-to-max-drawdown ratio, all powered by Claude AI, without ever touching Pine Script.

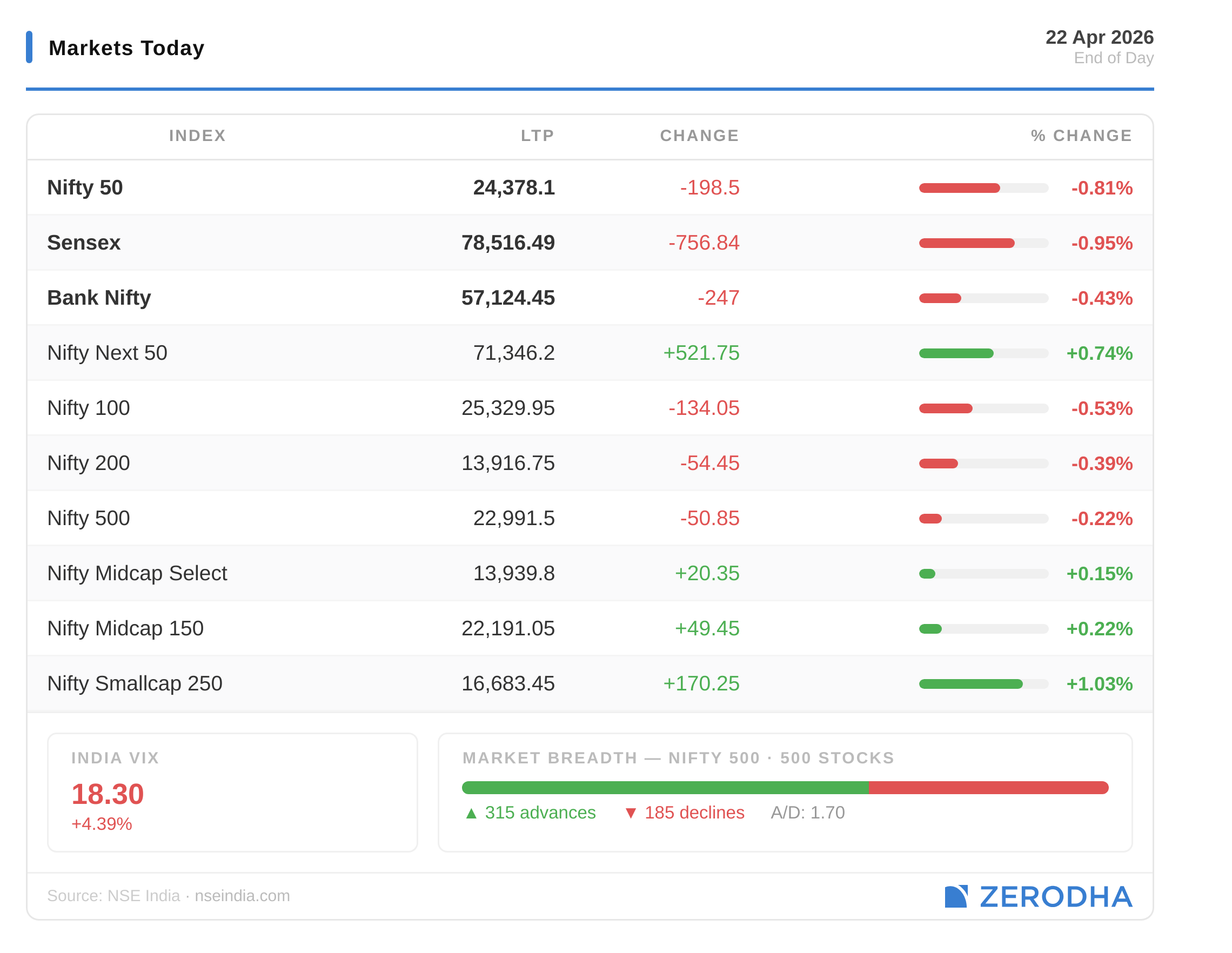

Markets Today

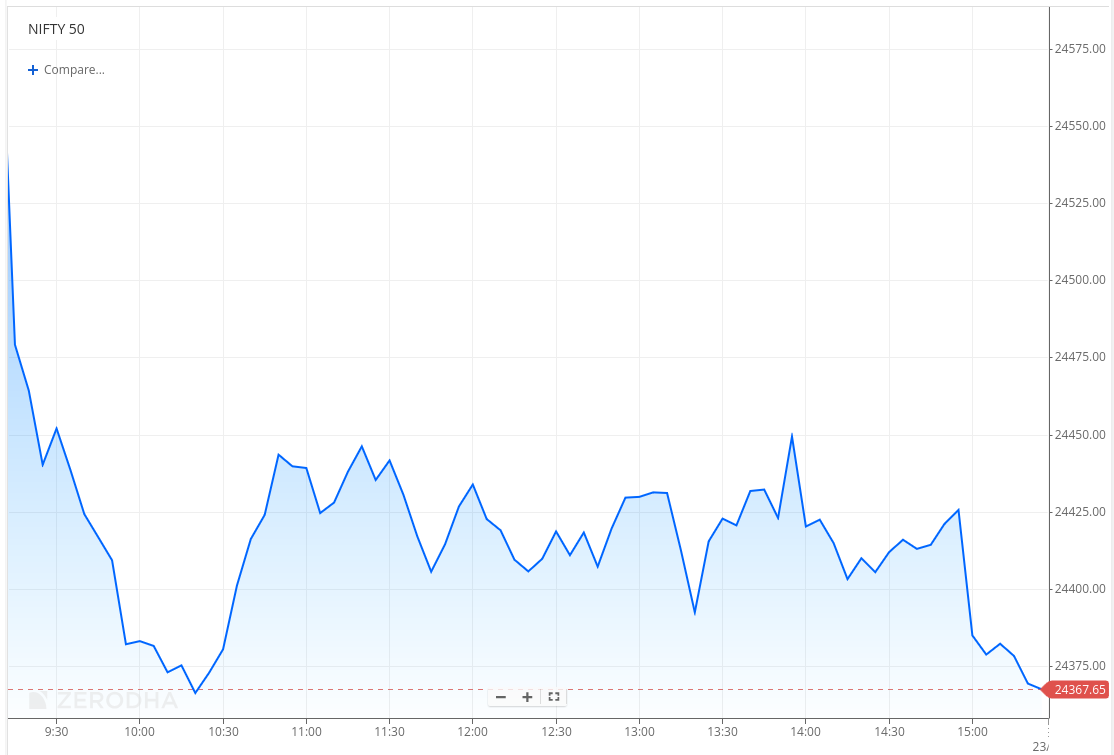

Nifty opened with a gap down of 106 points at 24,471, tracking weakness in IT stocks following disappointing results, along with a spike in crude oil prices. The index came under immediate selling pressure, slipping steadily toward the 24,350–24,380 zone within the first hour.

After the early decline, Nifty saw a mild recovery in the late morning, moving back toward the 24,400–24,450 range. However, the bounce lacked conviction, and the index remained choppy with no clear direction till noon.

In the second half, Nifty continued to oscillate in a narrow 24,400–24,450 band, with repeated attempts to move higher getting sold into. A brief spike toward 24,450 around 2 PM was quickly reversed, keeping the index under pressure.

Selling picked up again in the final hour, dragging the index back toward the 24,360–24,380 zone. Nifty eventually closed at 24,378.10, marking a weak session defined by early selling, lacklustre recoveries, and renewed pressure into the close.

Nifty fell 198 points (-0.81%), while Sensex declined 0.95% and Bank Nifty slipped 0.43%. Despite the weakness, market breadth favoured advances (315 vs 185), but VIX rose 4.4% to 18.3, indicating underlying caution.

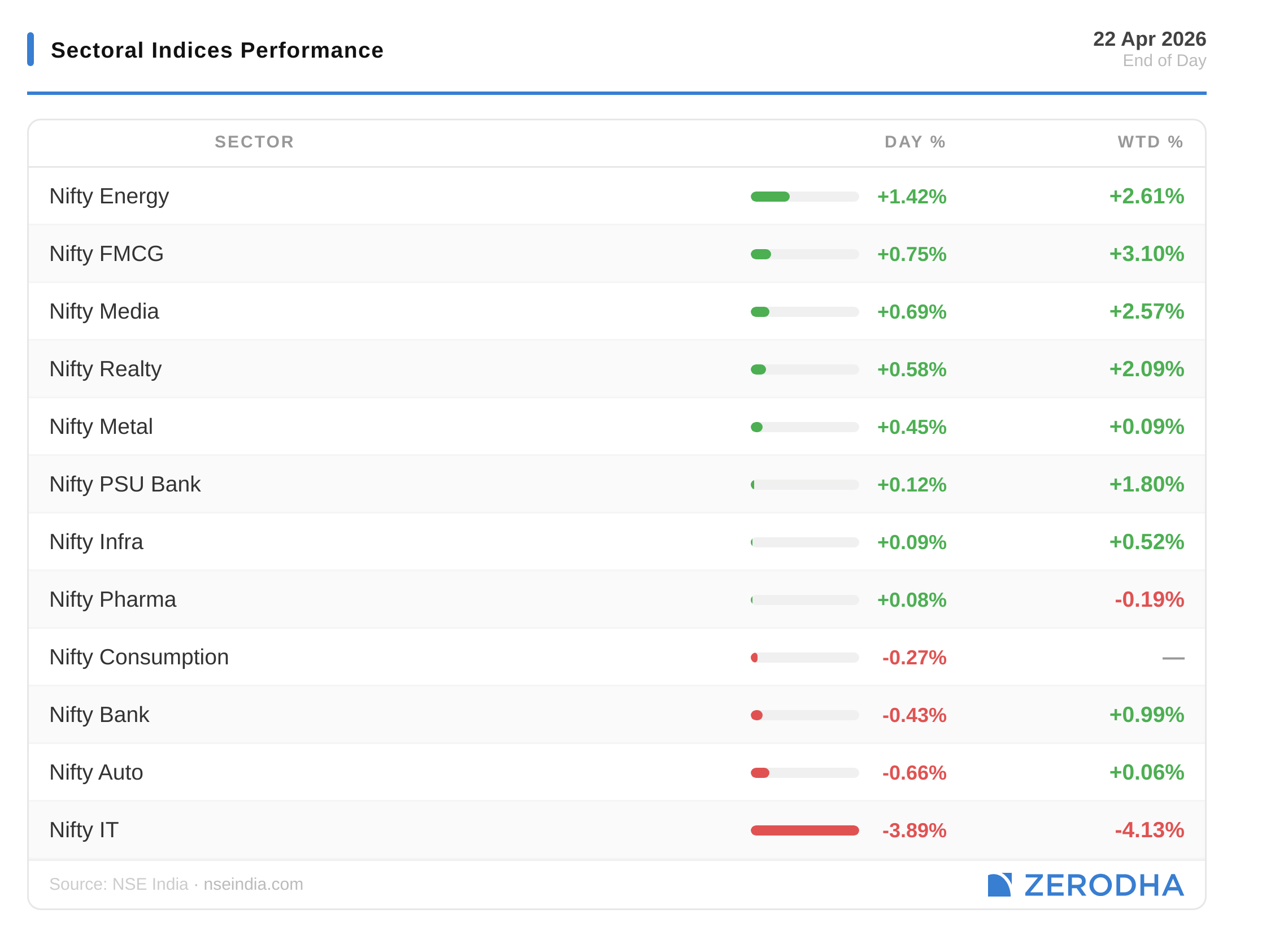

Sectoral Indices Performance

Energy ripped 1.42%, FMCG added 0.75%, Media and Realty both climbed above half a percent. IT crashed 3.89%, dragging the headline indices down. Auto and Banking both bled, falling 0.66% and 0.43% respectively.

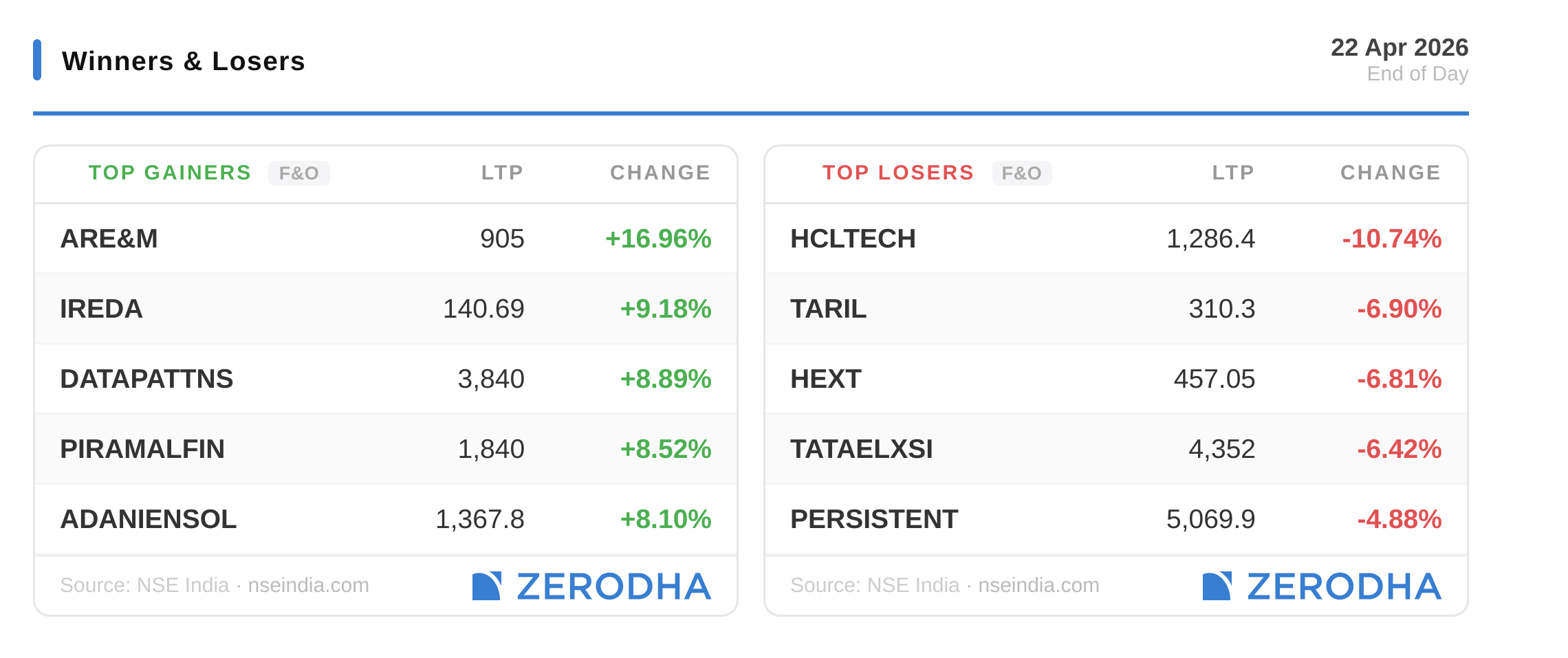

Winners & Losers

Midcap bucked the trend, rising 0.15% while Nifty sank. Eight of twelve sectors closed green, and breadth stayed positive despite heavyweights bleeding. Small divergence between large and mid is widening.

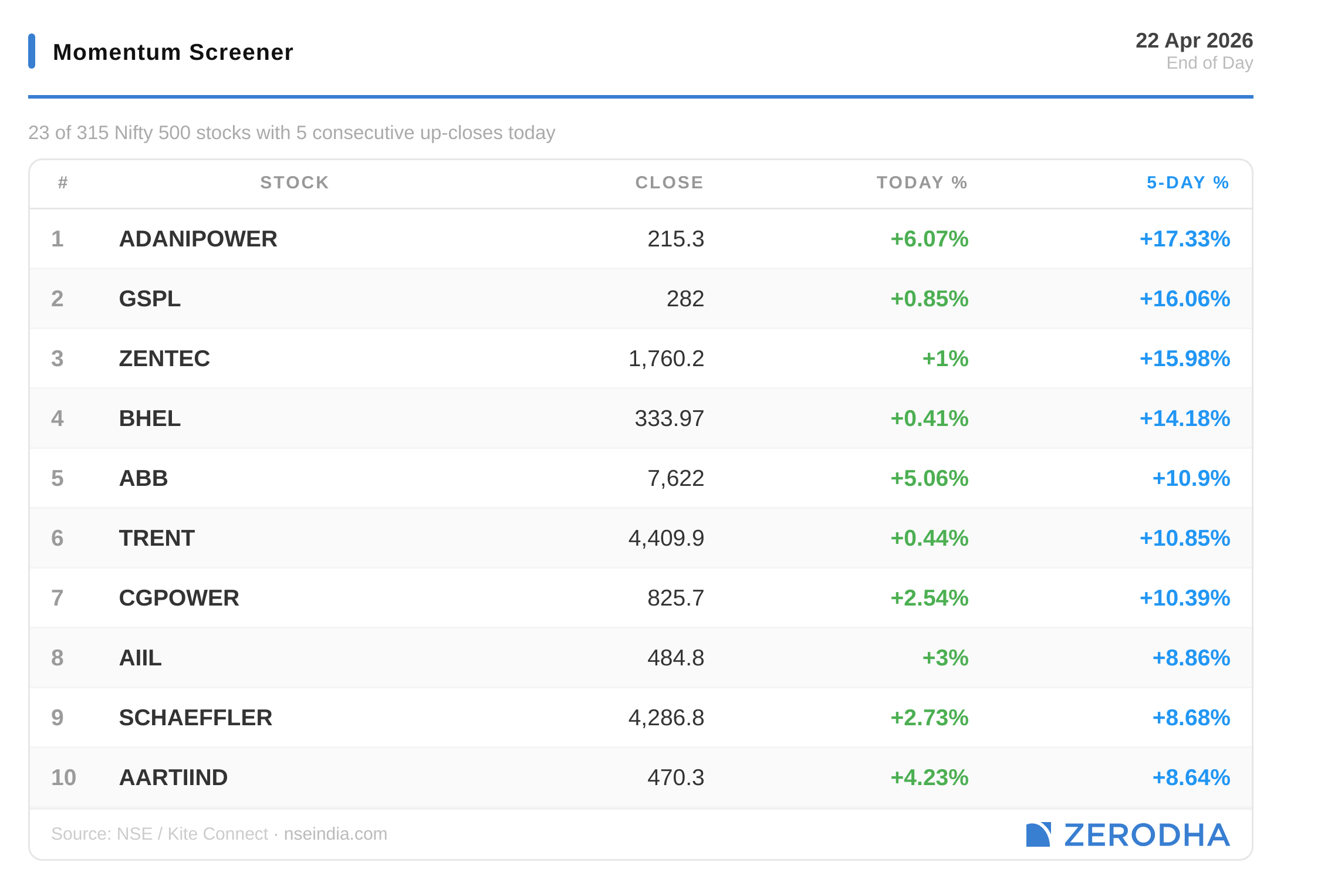

Momentum Screener

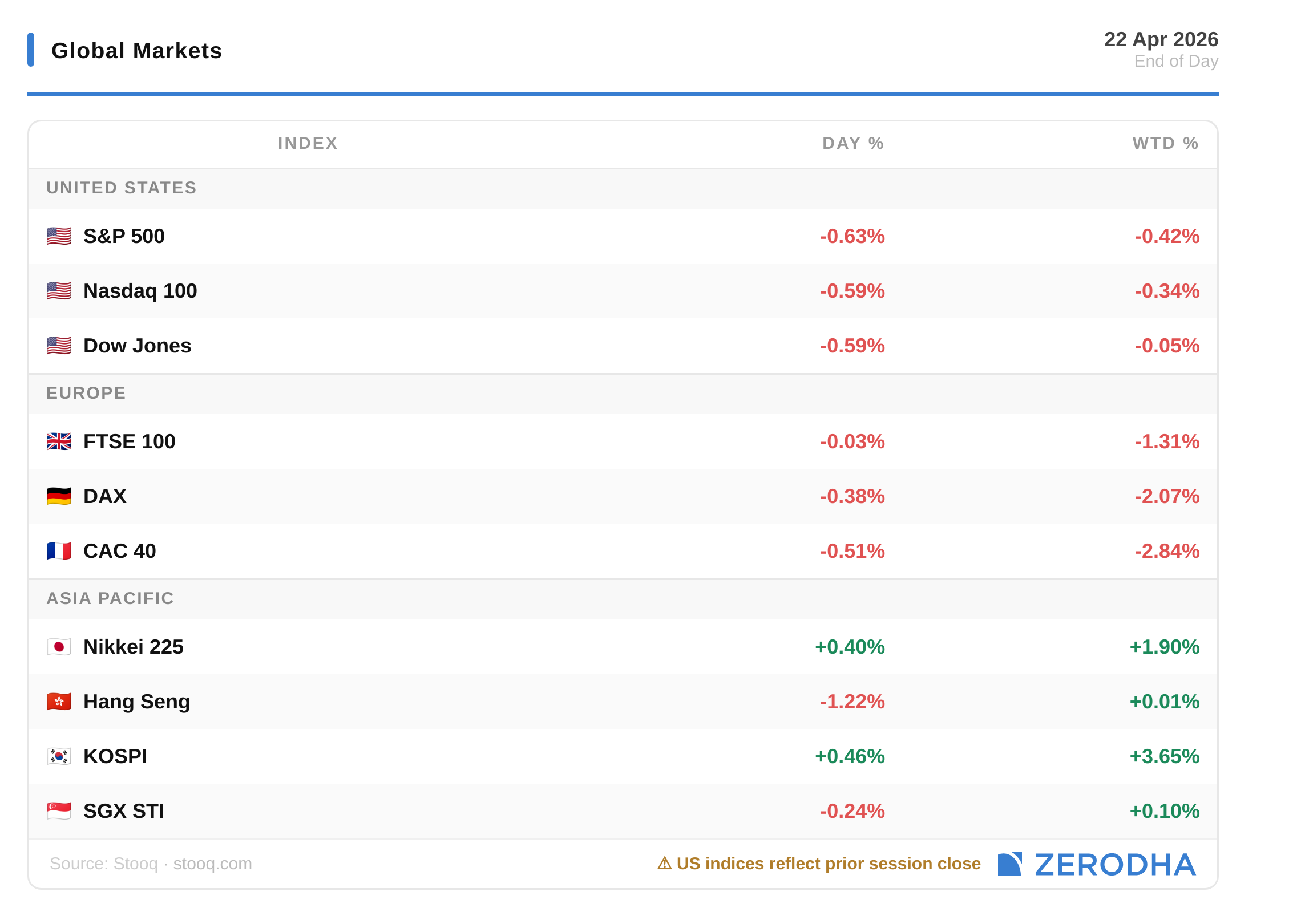

Global Markets

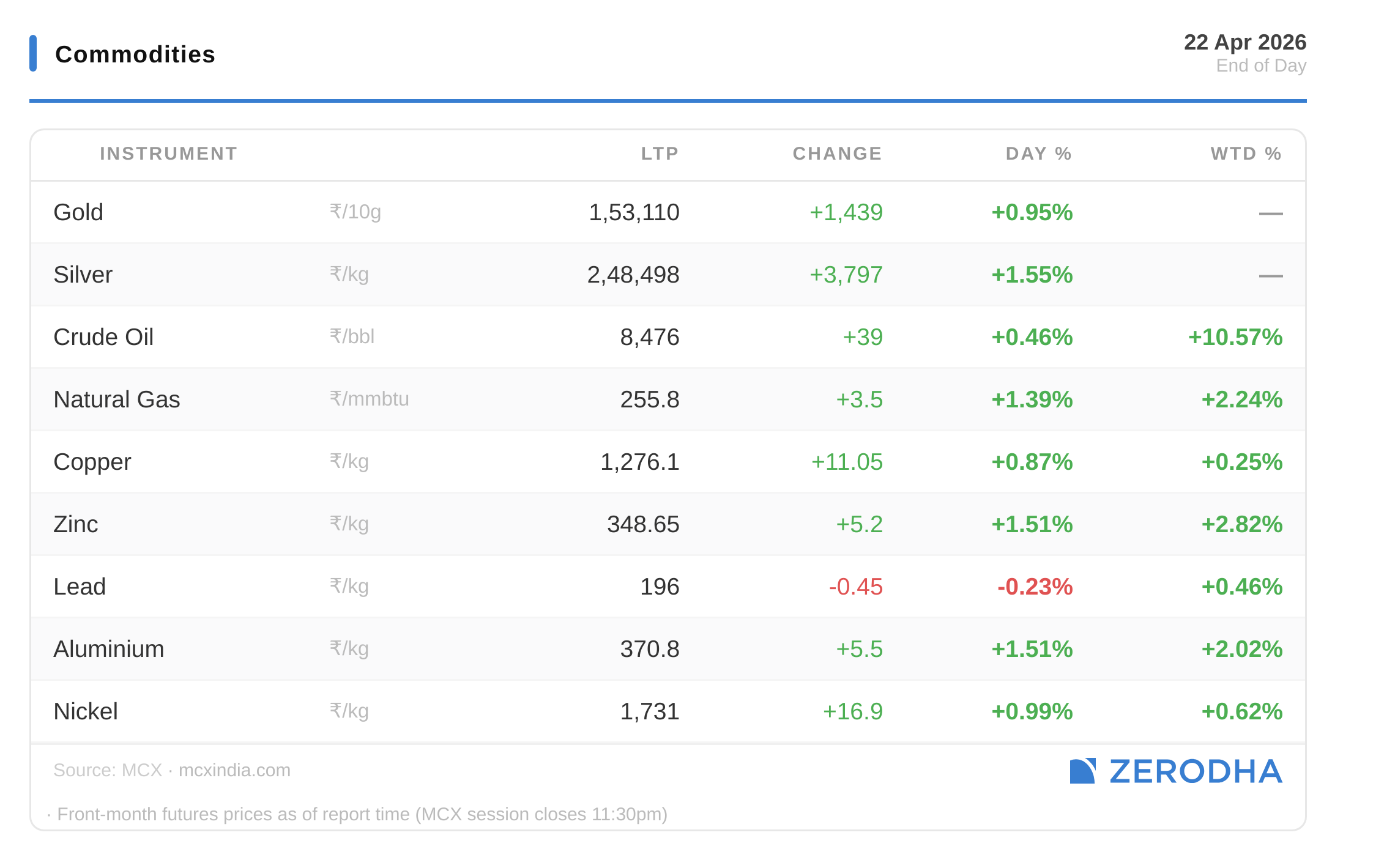

Commodities

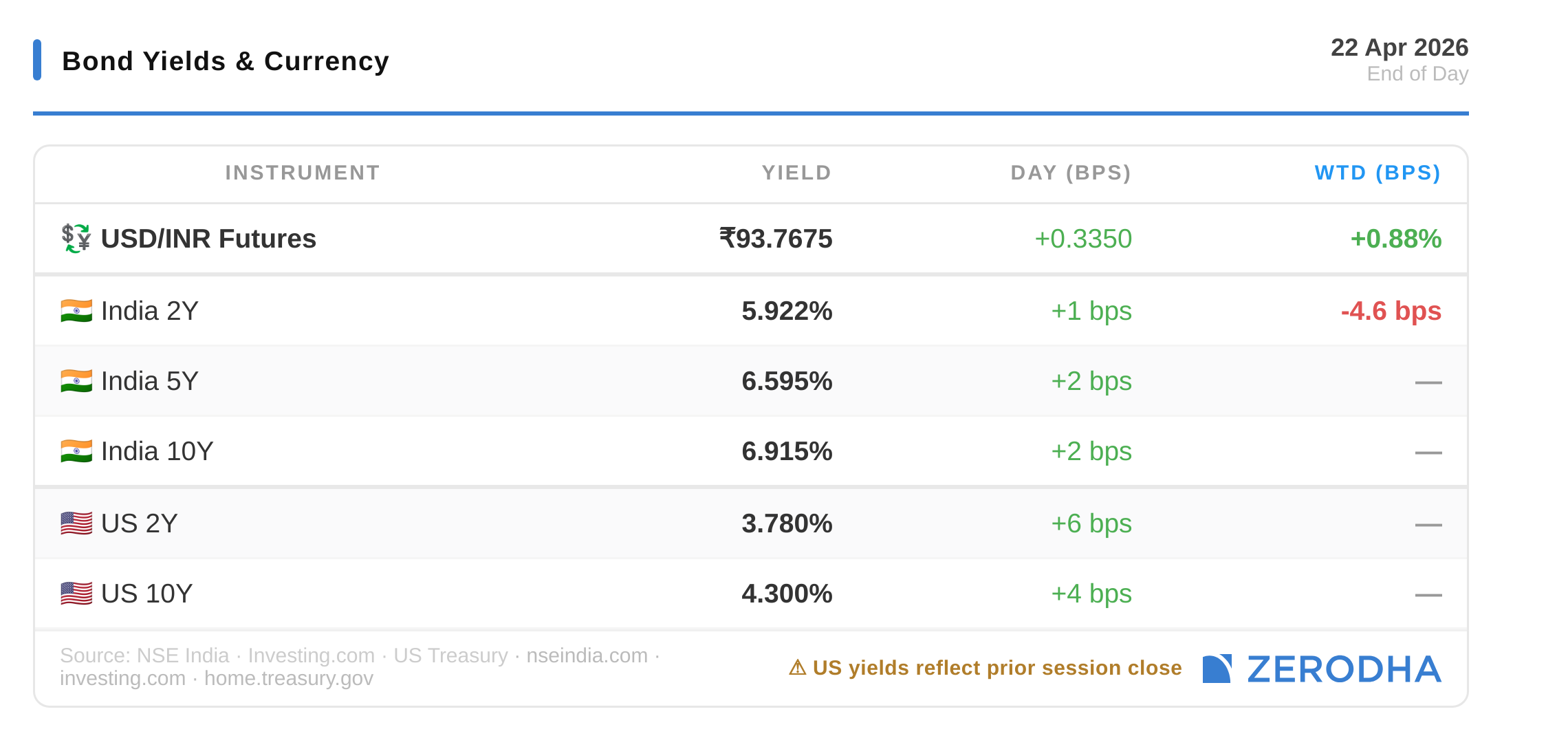

Bond Yields & Currency

India 10Y yield at 6.915%, US 10Y at 4.3%. Rupee weakened 0.36% to 93.77, tracking dollar strength and FII outflows.

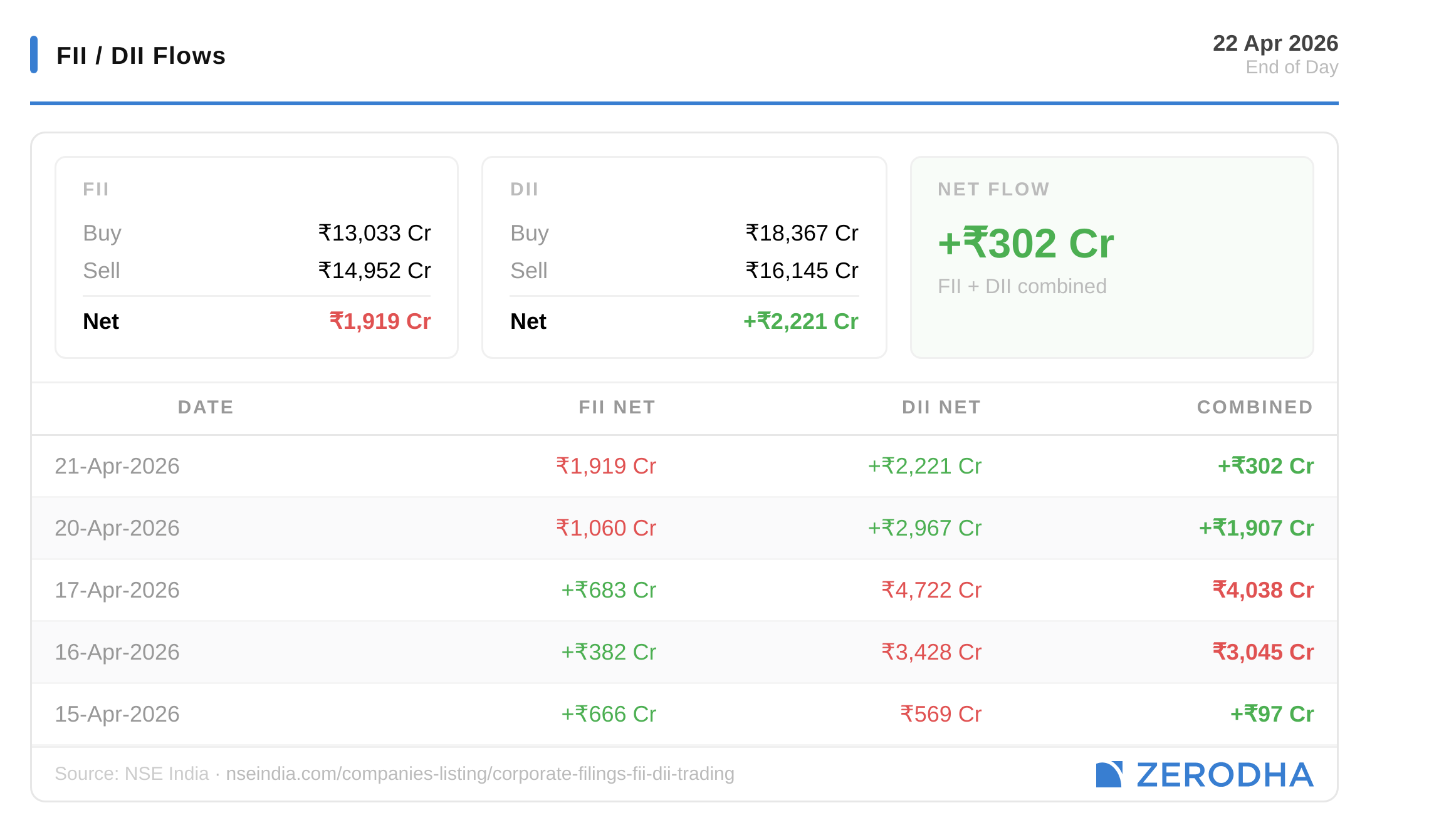

FII / DII Flows

Here’s the trend of FII-DII activity from the last 5 days:

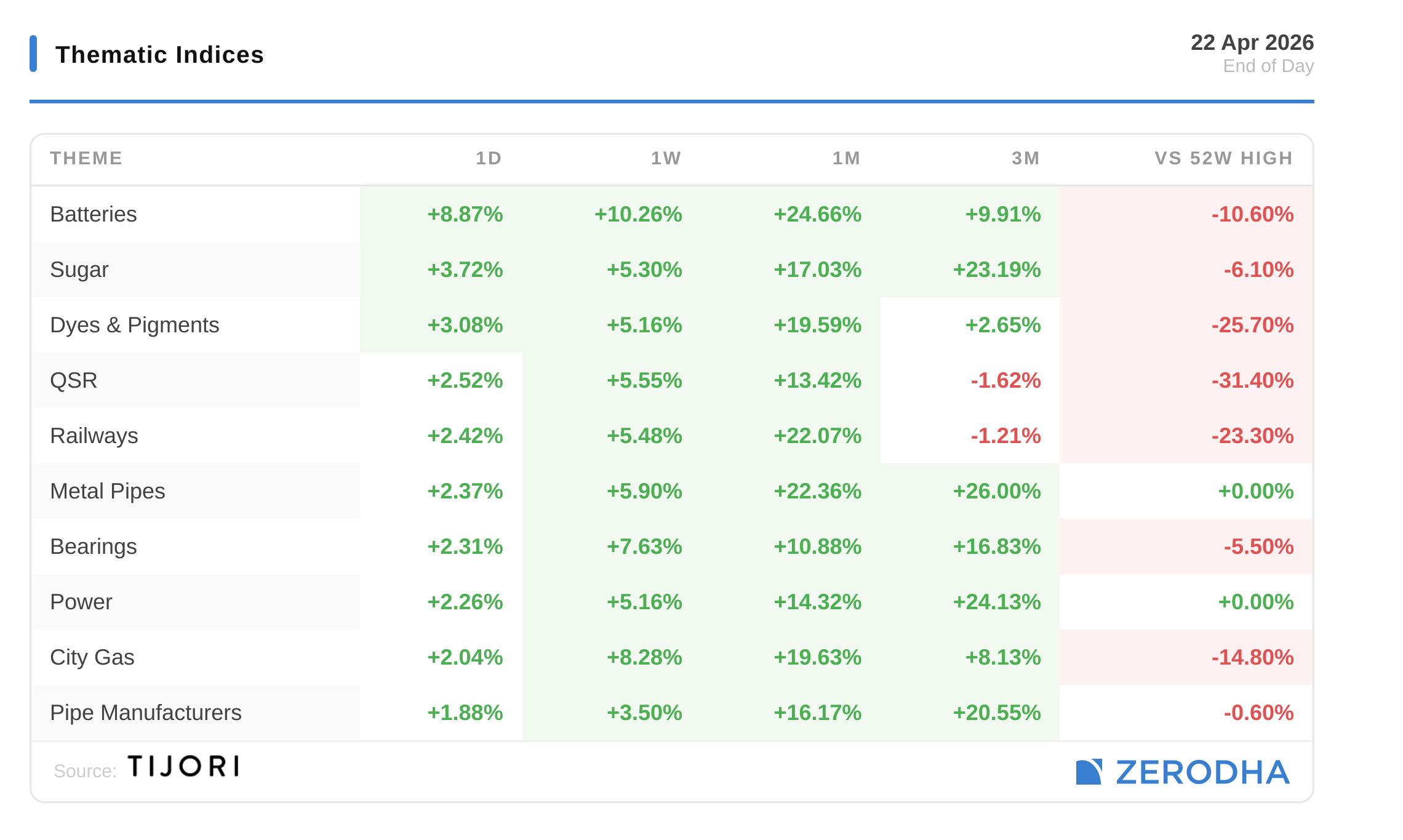

Thematic Indices

Tijori’s niche indices, where pockets of the market beyond standard sector baskets are sorted by today's move. You can also track the Promoter buying and other interesting stuff, like Capex activity by the companies in the Tijori App’s idea dashboard

Change in OI for the day

The following is the change in OI for Nifty contracts expiring on 28th April:

The maximum Call Open Interest (OI) is observed at 24,500, followed by 24,400, indicating potential resistance at the 24,500 -24,600 levels.

The maximum Put Open Interest (OI) is observed at 24,000, followed by 24,400 & 24,500, suggesting support at 24,100-24,000.

Note: OI is subject to multiple interpretations; however, generally, an increase in Call OI indicates resistance in a falling market, while an increase in Put OI indicates support in a rising market.

Source: Sensibull

Top Stories in India

HCL Technologies fell nearly 11% after it reported Q4FY26 profit of ₹4,488 crore, up 10.1% QoQ but just 4.2% YoY, with revenue growth remaining muted. Margins fell sharply to 16.5% due to weak discretionary spending, deal delays, and a decline in software revenue, while FY27 guidance of 1–4% growth signalled caution. Dive deeper

Tech Mahindra posted a strong Q4 with profit up 16% YoY to ₹1,354 crore and revenue rising 13%. Sequential momentum improved with EBIT up 10.2%, and the company declared a ₹36 per share dividend. Dive deeper

India’s textile exports grew 2.1% in FY26 to ₹3.16 lakh crore, supported by steady global demand. Ready-made garments remained the largest contributor, rising 2.9% YoY. Dive deeper

PNC Infratech emerged as L1 bidder for NHAI projects worth ₹3,483 crore, with execution timelines of two years for each project. Dive deeper

Larsen & Toubro subsidiary signed a long-term deal with ITOCHU Corporation to supply 3 lakh tonnes of green ammonia annually, supporting global maritime decarbonisation efforts. Dive deeper

Transformers and Rectifiers India shares dropped 7% after Q4 profit fell 5% YoY to ₹89 crore, despite a 16% rise in revenue, alongside a ₹0.25 dividend announcement. Dive deeper

India’s life insurance sector saw strong momentum in FY26, with new business premium (NBP) rising 15.7% to a record ₹4.59 lakh crore, crossing the ₹4 lakh crore mark for the first time, according to Life Insurance Council. Dive deeper

SBI Life Insurance Company reported a marginal 1.1% YoY decline in Q4 profit to ₹804.6 crore, despite strong premium growth of 16% to ₹27,684 crore. Sequentially, profit surged sharply, driven by a higher policyholder surplus. Dive deeper

Top Stories Globally

US President Donald Trump extended the Iran ceasefire while awaiting a unified proposal from Tehran. Despite this, the US continues its blockade of Iranian ports, signalling ongoing tensions. Dive deeper

Brent crude rebounded to around $100/bbl after fresh attacks on shipping near Iran, including vessels linked to the Strait of Hormuz, raising renewed concerns over supply disruptions. Dive deeper

GE Vernova raised its 2026 revenue forecast to $44.5–45.5 billion from $44–45 billion, driven by strong demand from data centres. The upgrade reflects accelerating order growth across its power and electrification businesses. Dive deeper

The dollar index eased slightly below 98.3, trading near pre-war levels as markets balanced ceasefire optimism with persistent geopolitical uncertainty. Dive deeper

South Korea’s benchmark KOSPI rose 0.46% to a record close of 6,418, driven by renewed buying in tech and industrial stocks after recent profit-taking. Gains were supported by optimism in AI and semiconductor sectors, particularly on expanded LG–Nvidia collaboration. Dive deeper

Management Chatter

In this section, we highlight interesting comments from the management of major companies and policymakers in the Indian and Global Economies.

C Vijayakumar, CEO & MD of HCL Tech, on continued softness in discretionary spending and client-specific delays:

Specifically, in the March quarter, we saw a slowdown in procurement decisions in the software business, which contributed to lower performance than expected. In services, there was a slowdown in discretionary spend, especially towards the end of the quarter.

I would not broad-brush it across sectors. These were client-specific situations—two in telecom and two in the SAP programme. North America remains robust; Europe is a little soft. There is no broader macro impact to call out. - Link

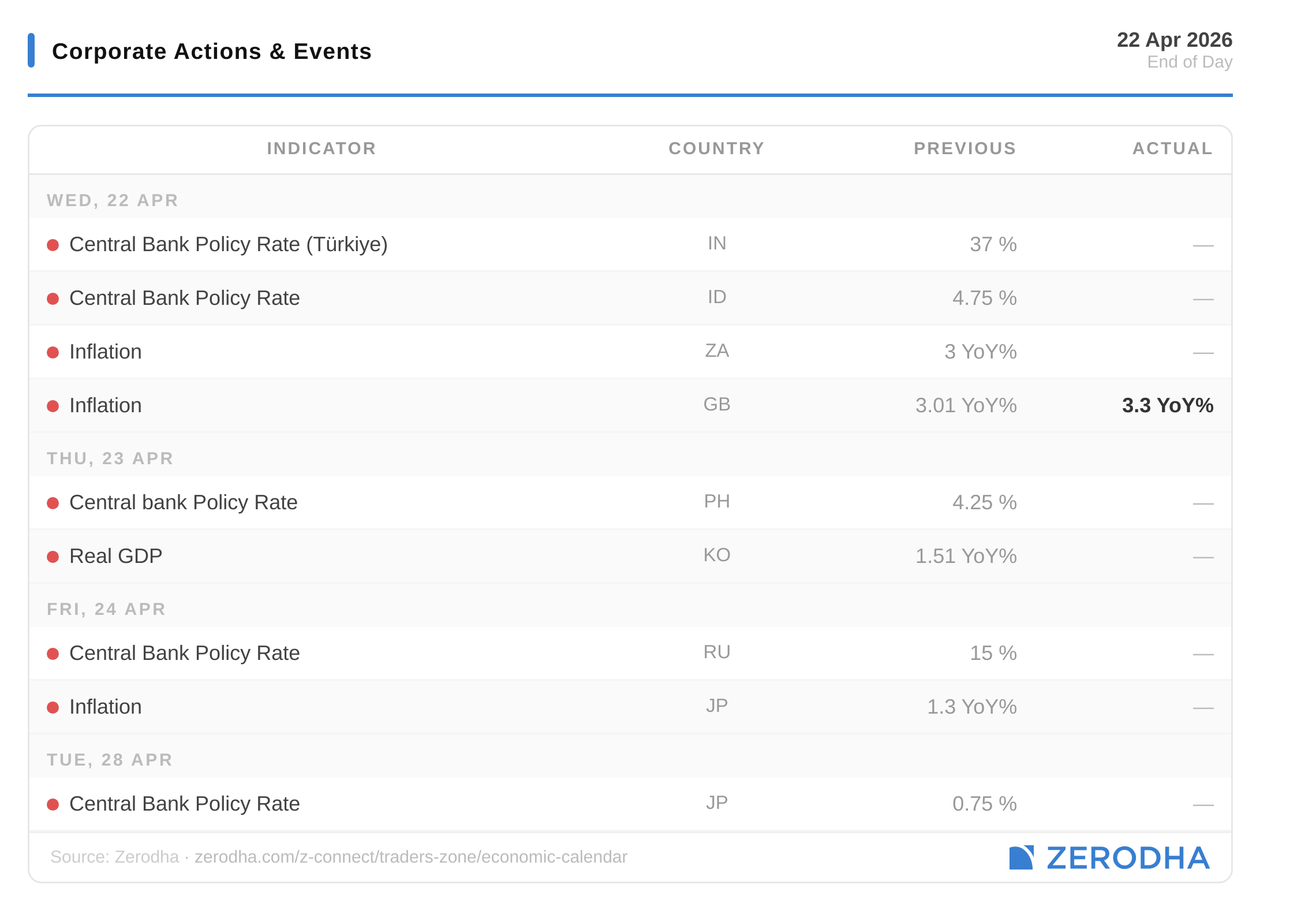

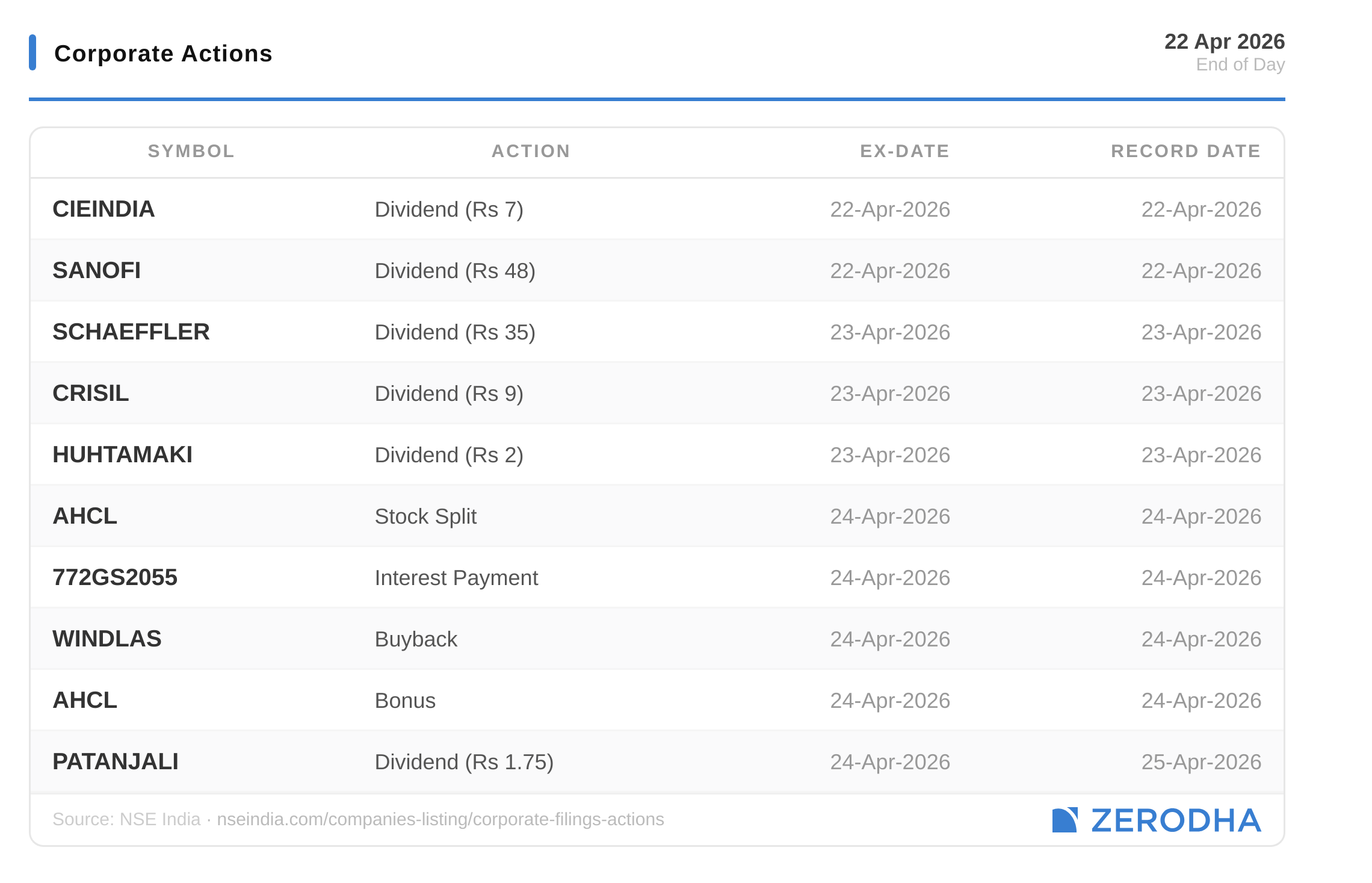

Corporate Actions & Events

Corporate Actions

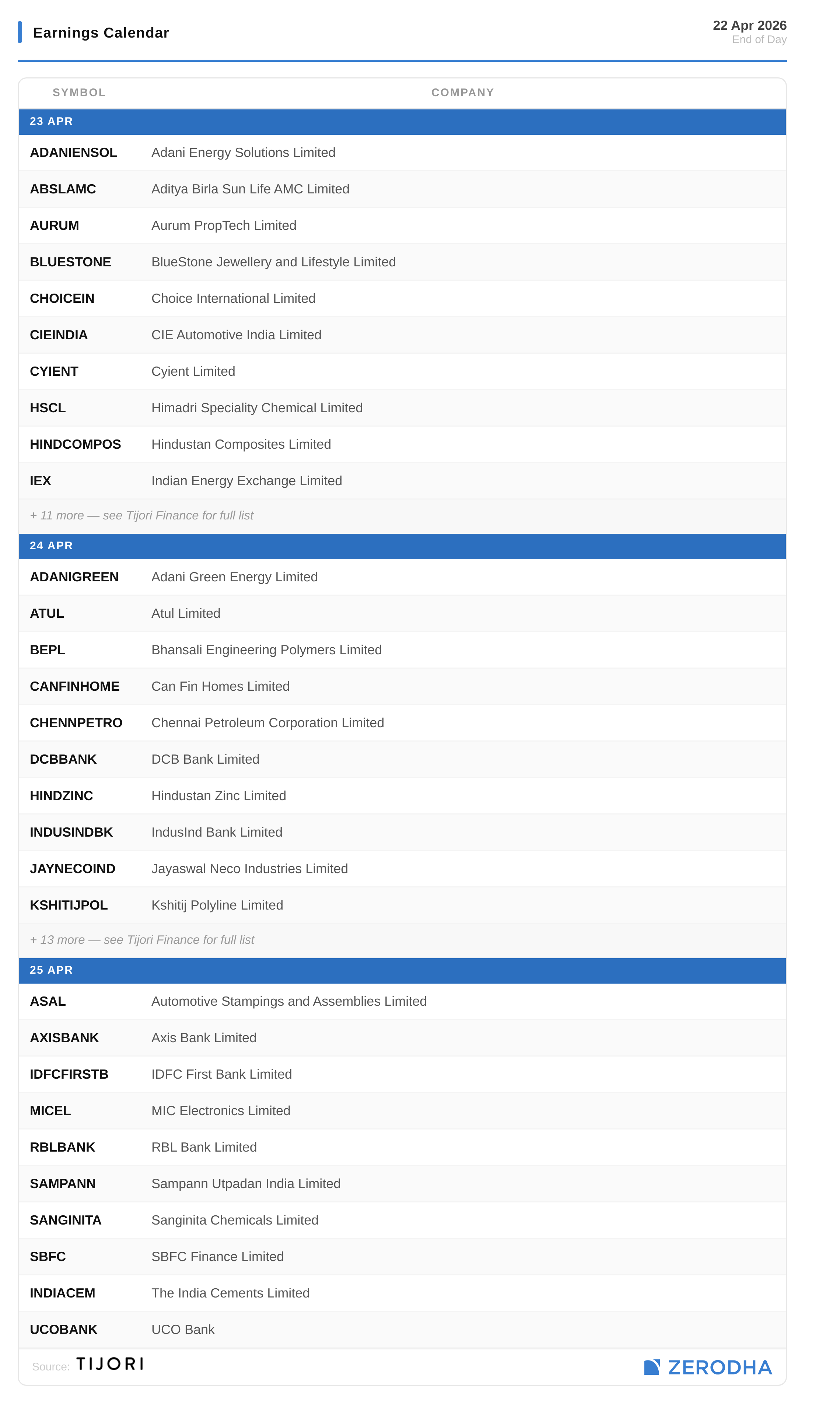

Earnings Calendar

Published by Zerodha. Not investment advice. Data from NSE, BSE, MCX.

That’s it from us for today. We’d love to hear your feedback in the comments, and feel free to share this with your friends to spread the word!

What are your views on E85 and E100 draft policy? Also, how much impact would we see in Sugar Industries due to this policy?